The plain definition

A trading edge is a repeatable, measurable advantage: across a large enough sample of trades, your approach makes more than it loses. The technical name for it is positive expectancy — what one average trade is worth, once wins and losses are weighed together:

Expectancy = (win rate × average win) − (loss rate × average loss)

If that number is positive over a large enough sample, you have an edge. If it is negative, you do not, no matter how good any single trade felt. Everything else people mean by "edge" — a setup, a market, a routine — only matters insofar as it pushes that one number above zero and keeps it there.

Win rate is not an edge

The most common mistake is to treat win rate as the edge. It is not. Consider two hypothetical traders, each over a large sample:

- Trader A wins 70% of the time, but the average loss is three times the average win. Expectancy is negative. A high win rate, and no edge.

- Trader B wins 40% of the time, but the average win is three times the average loss. Expectancy is positive. A low win rate, and a real edge.

Win rate is one of four inputs, and on its own it tells you almost nothing. This is why a 40%-win-rate system can compound an account while a 70%-win-rate system quietly drains it. The risk/reward calculator makes the relationship concrete: enter a reward-to-risk ratio and it returns the break-even win rate, the threshold above which an edge exists at all.

The two kinds of edge

When traders say "edge," they usually mean one of two different things:

Strategy edge

A setup, market condition, or structural inefficiency with positive expectancy. This is what a backtest measures.

Behavioral edge

Whether you actually execute that strategy as designed, trade after trade. This is what a journal measures.

The two are not the same, and the gap between them is where most retail accounts are lost. A strategy can have a real edge on paper and still lose money in practice, because the person trading it sizes up after a win, chases an entry out of fear of missing out, or slides a stop to avoid taking the loss. The paper edge survives; the executed edge does not.

A backtest measures the strategy edge. A journal measures the behavioral edge. They answer different questions, and a trader who already has a strategy is usually losing money to the second one.

Why you cannot see your edge by feel

Ask a trader where their edge is and most will answer from memory. Memory is the wrong instrument. A few vivid trades — the big win, the painful blowup — dominate the sense of what works, while the long tail of ordinary trades that actually determine expectancy fades. Recency bias weights last week more than last quarter. Emotion tags the memorable trades, not the representative ones.

The edge is not in the highlight reel. It is in the full record, including the boring trades nobody remembers. That record is also where the behavioral edge hides, because the conditions under which a trader executes well are usually invisible from the inside. The published work on overconfidence and the disposition effect describes these blind spots in detail; the research page lists the studies Kyra is built on.

How to find your edge

Finding an edge is an act of measurement, not introspection. The method is the same whether the tool is a spreadsheet or an app:

- Log every trade.Not the memorable ones, every one. A partial log is biased toward whatever was vivid, which is exactly the bias you are trying to escape.

- Give it a sample.Expectancy on five trades is noise. The number stabilizes only as the sample grows, which is why an honest early estimate comes with a wide range and a later one narrows. The math of that is in how many trades before patterns emerge.

- Break it down by condition.Overall expectancy is a starting point. The useful version is conditional: expectancy on planned setups versus impulsive ones, on calm trades versus anxious ones, by time of day. That is where an edge stops being a single number and becomes something to act on.

The honest version of this measurement always carries its uncertainty. A pattern that says your planned setups are profitable means more when it shows how many trades it is based on and how wide the range around the estimate still is. A point estimate with no sample size is a guess wearing a number.

An edge is not a feeling about your trades. It is a number, and the number needs a sample.

Edge versus leak

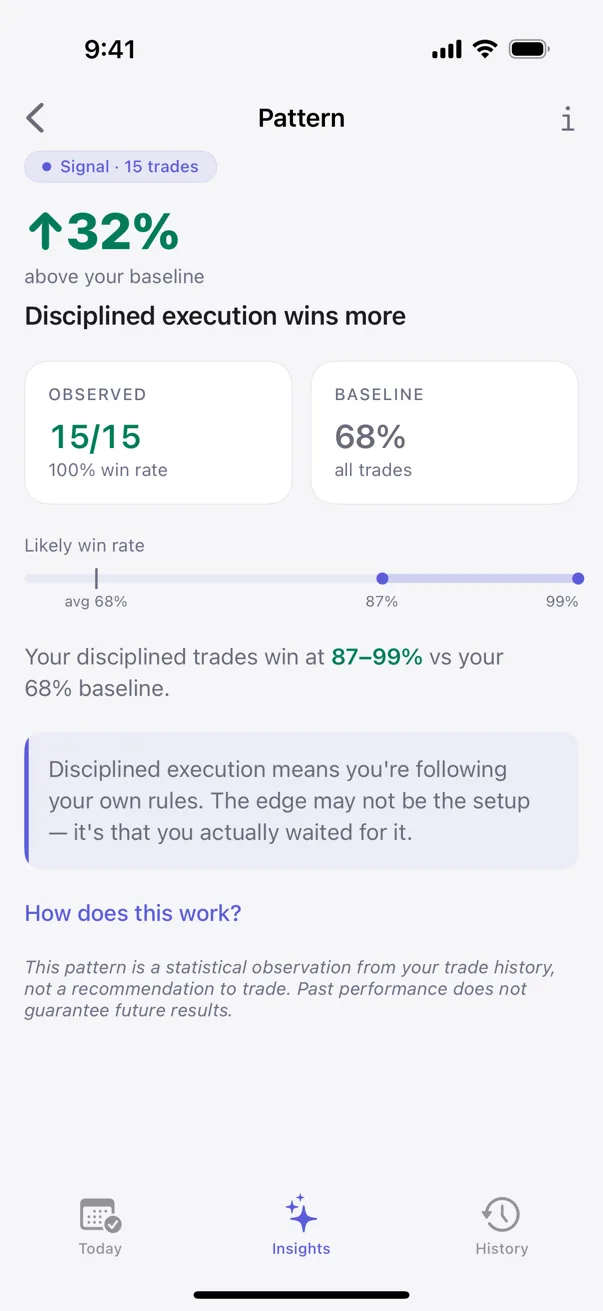

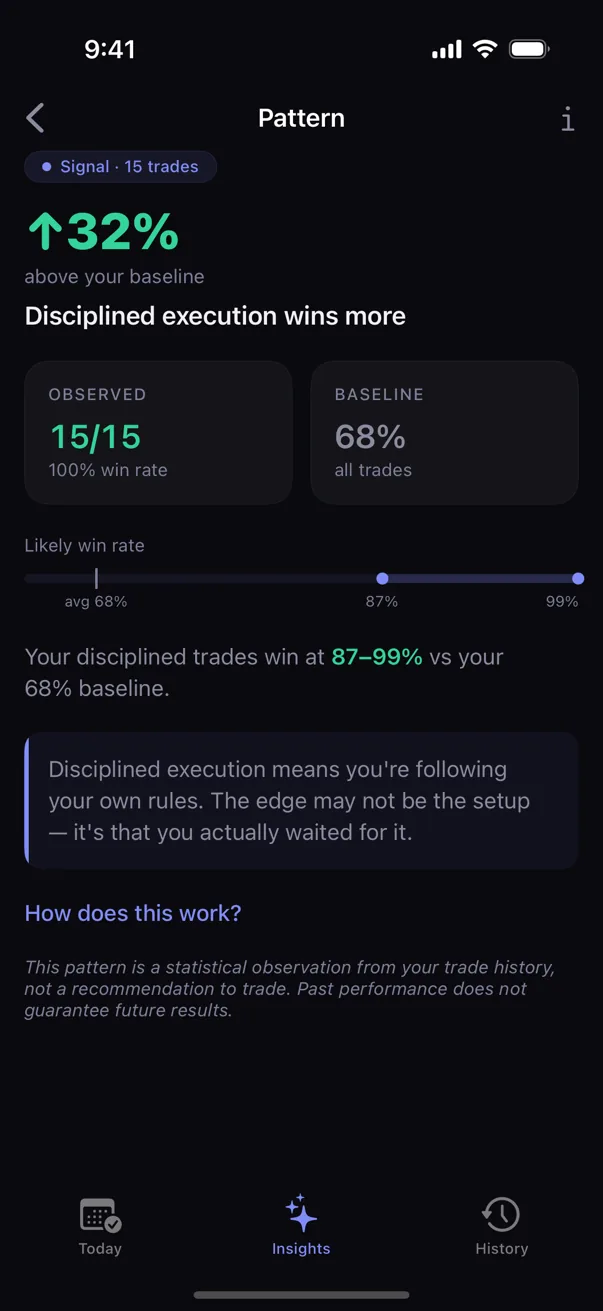

A trade history surfaces two kinds of conditional pattern. A leak is a condition where you reliably lose — the costly habit. An edge is a condition where you reliably do well — the repeatable strength. Most trading advice fixates on the leak, because fear is the louder motivator. But naming the edge first is more useful: it tells you what to do more of, not only what to avoid, and it is easier to lean into a strength than to white-knuckle a weakness out of existence.

A trader who knows that calm, planned, mid-morning entries are their strongest condition has something concrete to repeat. That is an edge expressed in their own behavior, derived from their own data rather than borrowed from someone else's playbook.

An edge is necessary, not sufficient

One caveat, stated plainly: an edge is necessary, not sufficient. A positive expectancy can still produce long losing streaks, and a real edge executed without discipline still bleeds. The edge is what makes discipline worth having; it does not replace it. No journal, Kyra included, can promise a profitable account. What a journal can do is make the edge visible, so the discipline has something true to protect.

Kyra surfaces your strongest detected pattern as your edge, with the sample size and an uncertainty range on the card. For how that detection works, see pattern detection and the math behind Kyra.