The trait myth versus the behavior reality

Ask most traders to define discipline and they describe a kind of person: someone steady, someone who does not flinch, someone who has it the way other people have brown eyes. The framing is comfortable because it explains every failure in advance — you broke your plan because you are not a disciplined person, and there is nothing to be done about that except wish you were someone else.

That framing is wrong, and it is wrong in a way that makes it useless. A trait is fixed and unmeasurable. A behavior is neither. Discipline is not who you are; it is what you did, and how often. Specifically, it is the share of your trades that followed the plan you set for them — entry on a setup you had decided to take, size you had decided to use, stop you had decided to honor.

The moment you state it that way, two things change. First, it becomes a number: out of your last forty trades, how many followed the plan and how many did not. Second, it becomes movable — you can run the number up the same way you run any rate up, by changing the conditions under which the next trade happens. A trait you are stuck with. A rate you can work on.

"Am I a disciplined person?"

Fixed, unmeasurable, unfalsifiable. Every broken rule confirms it; nothing can change it. The question has no answer you can act on.

"How many trades followed my plan?"

A rate, countable from the log. Some trades did, some didn't. The gap is visible, and the conditions that produced it can be changed.

Why willpower fails

The trait story has a sibling: the idea that discipline is willpower, a reserve of grit you draw on to force the right decision in the moment. If you just want it badly enough, you will hold the line. This is the advice in most trading psychology, and it fails for a reason the research made clear decades ago.

Willpower is depletable. In the experiments that established the effect — whose effect size is still debated — Baumeister and colleagues showed that exerting self-control on one task left people measurably worse at self-control on an unrelated task that followed — they named it ego depletion [1]. The active, regulating self behaves like a limited resource: spend it resisting one urge and there is less left for the next. A trading session is a long string of exactly those urges. The trader who has white-knuckled past five marginal setups is not the same regulator at the sixth, and willpower budgeting is not a plan you can hold a session on.

This is the same fault line that runs under the two best-documented discipline failures. Revenge trading is what happens when a loss spikes stress and the in-the-moment self, cognitively impaired, reaches for the next trade to undo the last one. Overtrading is what happens when boredom, a win streak, or a recovery urge quietly loosens the criteria and the marginal trade slips through. Both are specific instances of the same general fact: the person making the decision in the moment is not the person who set the rule, and is in worse shape to keep it. Asking the impaired self to summon willpower is asking the wrong self at the wrong time.

Discipline as plan-adherence

If discipline is a rate, you need to define what counts as a hit. The operational definition is plan-adherence: a trade adheres if it did what you had decided in advance it would do. Three checks cover most of it. Was the entry a setup you had planned to take, or one you reached for? Was the size the size you had set, or did it drift to fit a feeling? Was the stop the one you had defined, honored as defined, rather than widened or pulled? A trade that clears all three followed the plan. A trade that misses one or more did not — regardless of how it turned out.

That last clause is the whole point, and it is the hardest to internalize. Plan-adherence is a process measure, not an outcome measure. A trade can break every rule and still win; a trade can follow the plan perfectly and still lose. Outcome is noisy in the short run because the market gets a vote. Process is the part you control, and it is the part worth scoring. Steenbarger's case for trading as a performance discipline rests on exactly this shift — from chasing best outcomes to building best processes, because the process is what is repeatable and the outcome is what is not [2].

Scored over enough trades, the rate is also diagnostic. Bin your trades by how well they followed the plan and look at how each bin performed. The shape that tends to emerge is the one below: the trades that followed the plan carry the expectancy, the partial-adherence trades give some of it back, and the deviations — the reaches, the size drifts, the pulled stops — are where the damage concentrates. The figure is illustrative, but the relationship it draws is the one the process argument predicts.

Systems beat willpower

If the in-the-moment self cannot be trusted to supply discipline, the pre-market self has to supply it instead — as structure the later self runs into rather than resolve it has to find. This is the same move the revenge-trading and overtrading fixes make, generalized: rules, checklists, and limits set while you are calm, enforced when you are not.

1. Set the rule when you can think

A rule is only worth anything if it was written when the regulator was fresh. Decide before the open what setups the day will take, what size each gets, and where the stops sit. Size each planned setup in advance with a risk/reward calculator so the number is locked to the trade's geometry, not to how the morning feels. The pre-market self does the thinking; the in-trade self only has to obey a decision already made.

2. Make the rule binary

The best rules remove the judgment call from the moment your judgment is most degraded. A daily loss limit, a trade quota, a pre-defined setup list — each is binary. Either the trade is on the list or it is not; either you have trades left or you do not. There is nothing to decide in the moment, which is exactly the point, because deciding in the moment is what fails.

3. Close the loop by reviewing

Reps alone do not build skill. Deliberate practice does — and the defining feature of deliberate practice, in the research that established it, is the feedback loop: structured repetition against a clear standard, with review that tells you where you missed [3]. Trading the same plan a hundred times teaches nothing if you never check which of the hundred followed it. The review is what turns a logged trade into a corrected one, and a missed rule into a tightened one. Without it, the rate never moves; with it, every session is a data point you can learn from.

Measuring your discipline

All of this depends on being able to see the rate, and self-narrative is a poor instrument for it. "I'm a disciplined trader" is exactly what the trader who deviated on a third of last month's trades believes — the felt sense and the log routinely disagree, and the log is the one with the timestamps.

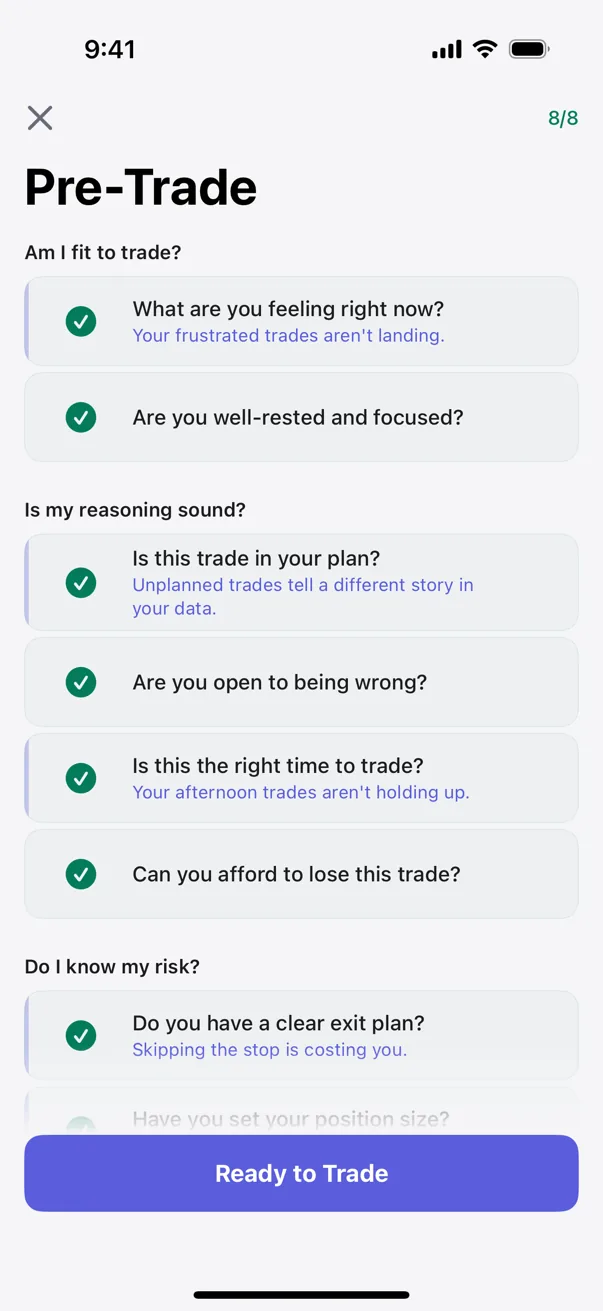

Kyra Trading is built to make plan-adherence visible. When you log a trade you mark whether it was a planned setup, and the pre-trade checklist captures the same intent — size, stop, the setup itself — before the trade goes live, so adherence is recorded at the moment it is honest rather than reconstructed afterward. Over time those marks become a rate you can watch: the share of your trades that followed the plan, trending up or down across weeks.

The engine then ties that rate to outcome. It bins your trades by adherence and tests whether the trades that followed the plan returned more than the ones that did not — using Bayesian inference and Fisher's exact test to separate a real effect from noise. Every pattern surface carries its sample size and a confidence range, so you can see how strong the signal is; patterns move through Tracking, Hint, Signal, and Proven tiers as the evidence accumulates. The output is not a verdict on your character. It is a measurement from your own money: your plan-adhering trades returned X more than your deviations. That number is harder to argue with than any feeling about whether you are a disciplined person.

Kyra runs this detection on-device. Nothing leaves your phone — no accounts, no servers, no shared data. The trader's data stays the trader's data. Discipline stops being a virtue you hope you have and becomes a number you can watch.

Sources

- Baumeister, R. F., Bratslavsky, E., Muraven, M., & Tice, D. M. (1998). Ego depletion: Is the active self a limited resource? Journal of Personality and Social Psychology, 74(5), 1252–1265.

- Steenbarger, B. N. (2015). Trading Psychology 2.0: From Best Practices to Best Processes. Wiley.

- Ericsson, K. A., Krampe, R. T., & Tesch-Römer, C. (1993). The Role of Deliberate Practice in the Acquisition of Expert Performance. Psychological Review, 100(3), 363–406.

Educational only. Not financial or trading advice. Behavioral patterns described above are observations from the published literature; specific outcomes vary with strategy, market conditions, and individual circumstances.