What revenge trading actually is

Revenge trading is the trade you would not have taken if the previous trade had won. The setup did not change. Your strategy did not change. The only thing that changed is the loss in your account, and the only reason you are in the next trade is to make that loss back.

Three things define the sequence:

- A recent loss — usually within the same session, often the same hour

- A compressed re-entry interval — minutes rather than hours

- Position sizing that does not match the setup — sized to recover the loss, not to fit the new trade's risk

If those three things line up, the next trade is almost never the one you would have taken on a fresh day. It is the trade your loss is taking, with you steering.

The trade you'd take

Entered on its own merits, sized to the setup's risk, stop where the chart says it goes. The previous trade gets no vote.

The trade your loss takes

Entered minutes later, sized to win the loss back, stop widened or skipped. Same chart — a different reason for being in it.

Why it happens — three behavioral mechanisms

Calling revenge trading a discipline failure misses the point. The behavioral finance literature has mapped the underlying mechanism for decades, and "willpower" is not on the list of fixes.

Loss aversion

Prospect theory [1] established that losses feel roughly twice as bad as equivalent gains feel good. This is not a metaphor — it is the slope of the value function in the original Kahneman and Tversky paper. A $500 loss does not register as the absence of $500. It registers as a wound that demands closing.

In trading, the closing mechanism is the next trade. The brain treats the loss as a reversible state, and the next trade is the lever. The math is wrong — the loss is realized regardless of what the next trade does — but the felt urgency is real.

Cognitive control degradation under stress

Research on trader physiology, notably John Coates' work on cortisol and risk-taking on a London trading floor [2], found that cortisol rose with the volatility and uncertainty of traders' P&L — and the broader stress literature ties elevated cortisol to degraded working memory, impulse inhibition, and time-horizon estimation, exactly the cognitive functions disciplined trading needs.

This is why "just don't do it" does not work. The person you are asking not to revenge-trade is not the same person who decided not to revenge-trade.

The "make it back" trap

Revenge trading is rationalized as a recovery strategy. It is not. The math is clear: a 5% account drawdown requires roughly 5.3% to recover; 10% requires 11.1%; 25% requires 33%; 50% requires 100%. The recovery percentages outpace the loss percentages, and they outpace them faster the deeper the loss.

A revenge trade is therefore the worst possible response to a loss. It increases the drawdown if it loses, and the recovery percentages compound against the trader. Even when revenge trades win, they reinforce a behavior that loses on average.

The fingerprint in your trade log

Revenge trades have a fingerprint. They look like this in the trade log:

- Trade N closes at a loss

- Trade N+1 opens within 5–30 minutes

- Trade N+1 is in a similar instrument or sector — the brain returns to the "scene"

- Position size on N+1 is equal to or larger than N

- Stop loss on N+1 is wider than usual or absent

This is not a hypothetical. It is the structure that behavioral pattern detection picks up. The "post-loss × short-re-entry-interval" pattern is one of the cleanest signals in retail trading data, because the timing alone is diagnostic. A trader does not need any qualitative tag like "I was tilted" — the timestamps tell the story.

Three checks to interrupt the cycle

These work because they do not require the post-loss trader to be disciplined. They require the pre-loss trader to set up rules that the post-loss trader will run into.

1. The 15-minute pause

After any loss, do not enter a new trade for 15 minutes. Walk away from the screen. The exact duration matters less than the principle: the post-loss decision-maker is impaired; give them time to reset.

This rule survives even when willpower fails because it is binary. Either 15 minutes have passed or they have not. There is no judgment call to make in the moment, and judgment in the moment is exactly what is degraded.

2. The pre-defined position size

Before market open, decide your position size for every trade today. Write it down. Use a position size calculator if the math feels fuzzy — the calculator's job is to lock in a number that does not depend on how the morning goes.

The post-loss trader cannot be trusted to size. The pre-market trader can. The calculator and the written number are how you make the post-loss trader obey the pre-market trader.

3. The hard daily loss limit

If you lose X% of your account in one session, you stop trading for the day. No exceptions. The number depends on your strategy — a common discipline-focused number is 2% per session, but use the risk/reward calculator to think through what your expected daily R looks like and where the limit should sit.

The point is not the number. The point is that the limit is set when you can think clearly, and enforced when you cannot.

Why most advice does not work — and what does

The internet is full of "do not revenge trade" advice. Trading psychology books are full of it [3]. Most of it is correct. Almost none of it is useful in the moment.

The reason: the advice assumes the trader can interrupt their own behavior in real time. The behavioral finance research above suggests they cannot — at least not reliably. The post-loss trader is impaired, and asking the impaired person to override their impairment is asking the wrong person.

What works is structural. Rules set in advance. Limits enforced by the platform or the calculator or the written plan. Process journaling that catches the sequence after the fact and surfaces it before it becomes habit.

This is also why measurement matters. A trader can know revenge trading is bad without knowing whether they do it. They can read every Steenbarger book and still not see their own pattern in their own data. The gap between "I know the rule" and "I can show you the trade where I broke it" is where the actual cost lives.

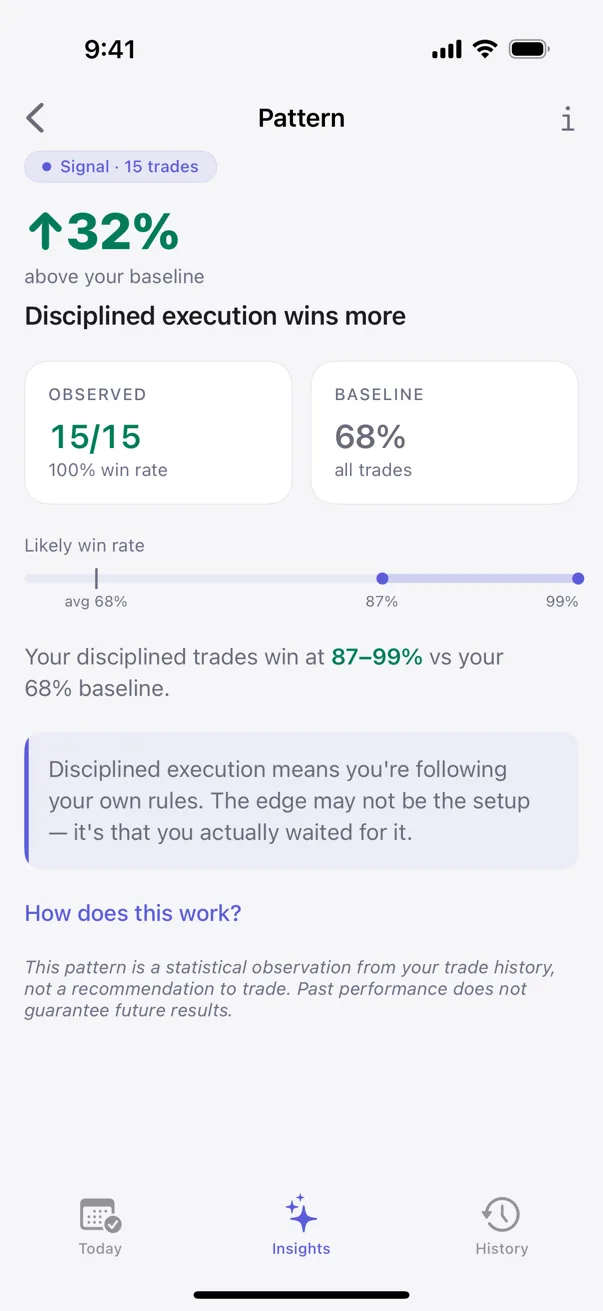

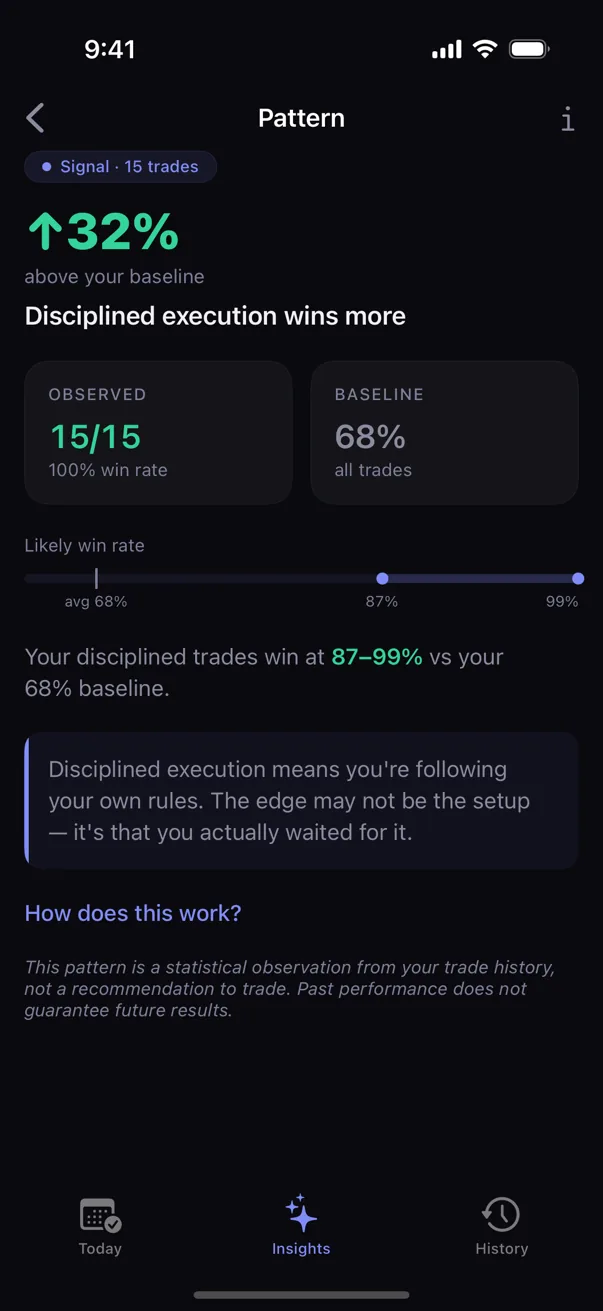

The measurement layer

Behavioral pattern detection — running statistical tests across a trader's own trade history — closes that gap. Specifically: the post-loss × short-re-entry-interval sequence is structurally identifiable. Once a trader has logged enough trades, the pattern can be detected automatically. The output is not a warning ("watch out for revenge trading"). It is a measurement ("the last 30 trades you took within 30 minutes of a loss returned X% less than your baseline"). That number is harder to argue with than a generic warning.

Kyra Trading is a private trading journal that does this detection on-device. Every pattern surface includes the sample size and a confidence range, so the trader can see how strong the signal is. Nothing leaves the device — pattern detection runs locally, no accounts, no servers. The trader's data stays the trader's data.

Sources

- Kahneman, D., & Tversky, A. (1979). Prospect Theory: An Analysis of Decision under Risk. Econometrica, 47(2), 263–291.

- Coates, J. M., & Herbert, J. (2008). Endogenous steroids and financial risk taking on a London trading floor. Proceedings of the National Academy of Sciences, 105(16), 6167–6172.

- Steenbarger, B. N. (2015). Trading Psychology 2.0: From Best Practices to Best Processes. Wiley.

Educational only. Not financial or trading advice. Behavioral patterns described above are observations from the published literature; specific outcomes vary with strategy, market conditions, and individual circumstances.