What tilt actually is

Tilt is a state, not an event. The word comes from poker, where a player who has taken a bad beat starts making decisions a clear-headed version of themselves never would — calling down hands they should fold, raising into spots they should pass, chasing the loss instead of playing the cards. The hands are different every time. The state behind them is the same: emotional arousal has overwritten the disciplined decision process, and the player keeps acting as if it hasn't.

The distinction that matters for traders is between the state and the behaviors it produces. Tilt is the impaired state; revenge trading is one specific behavior that the state produces. A trader on tilt might revenge-trade — but they might also oversize a perfectly valid setup, quietly loosen the stop they swore they'd respect, chase a name that already moved, or fire off three trades in the time they'd normally take one. Several behaviors, one underlying condition.

That is why "stop revenge trading" is necessary but not sufficient. You can defeat the revenge sequence specifically (the post-loss, compressed-re-entry, sized-to-recover trade covered in how to stop revenge trading) and still be on tilt — still rule-loosening, still oversizing, still chasing. The behavior is the symptom you can see. The state is the thing actually driving the next several decisions.

Tilt

A compromised decision process after an emotional trigger. It doesn't pick one behavior — it degrades the whole process for as long as it lasts.

Revenge trading

One specific output of the tilt state: the trade taken to win the last loss back. Defeating it doesn't end the tilt — oversizing, rule-loosening, and chasing are still on the table.

The physiology of tilt

Tilt is not a character flaw the disciplined trader has trained out. It is a physiological state, and the research on trader bodies has measured it directly. Treating it as a willpower problem misreads where the failure happens.

Lo, Repin, and Steenbarger's 2005 study of day traders [1] tracked traders' emotional states through daily surveys across live trading and matched them to each day's results. Traders who reacted most intensely to gains and losses performed measurably worse than peers with lower reactivity. Traders who reacted most strongly to market events, whose bodies spiked hardest on swings, performed measurably worse than peers with lower reactivity. The emotional response was not a side effect of bad trading. It tracked the bad trading directly, moment to moment.

Coates and Herbert's 2008 study on a London trading floor [2] measured the hormone underneath that reactivity. They found that elevated market volatility and uncertainty about outcomes raise cortisol — and that cortisol degrades exactly the cognitive functions disciplined trading depends on: impulse inhibition, working memory, and time-horizon estimation. The last one matters most for tilt. A trader flooded with cortisol doesn't just feel worse; they literally estimate time horizons differently, which collapses the patience a good setup requires into the urgency a bad one rewards.

This is the mechanism behind "I knew better." The trader did know better — when they set the rule, in a calm state, with their impulse control intact. The trade that breaks the rule is made by a body that has since been flooded, by a decision-maker whose inhibition and time sense have measurably degraded. "Just don't tilt" asks the impaired version of the trader to override their own impairment in real time. The research suggests that is the wrong person to ask.

What a tilt run looks like in your log

Tilt is a cluster, not a point. A single bad trade is noise; every trader has them on their best days. Tilt shows up as a run — a sequence of consecutive trades inside one session where three things move together:

- Size drifts up — positions creep above your baseline as the run goes on, sized to the feeling rather than the setup

- Stops loosen — the stop gets wider than usual, or moves after entry, or quietly stops being set at all

- An emotion tag coincides with below-baseline outcomes — the trades carry a frustrated, anxious, or hyped tag, and they return less than your calm-state trades over the same stretch

The trigger is usually visible at the front of the run — a hard loss, a missed move, a stop run that felt personal. What makes it tilt rather than a single reaction is the persistence: the next trade is worse, and the one after that, until something breaks the state. The recovery, when it comes, is often a break — time away from the screen, the session ending, a walk — not a trade that finally goes right.

The shape is the tell. One red bar is a bad trade. A run of red bars after a trigger, with size drifting up underneath them, is a tilt run — and unlike a feeling, the run is sitting in the log as timestamps and dollar amounts, whether or not the trader remembers being tilted at the time.

How to reset

The defenses that work share one property: they are set by the calm trader and enforced on the tilted one. None of them depend on the tilted trader recognizing their own state, because the research above says that recognition is exactly what's degraded.

- Step away — a hard rule, not a judgment call.After a trigger — a loss past a threshold you set in advance, or two losers in a row — you leave the screen for a fixed interval. Not "if I feel tilted." The whole problem is that the tilted trader is the worst judge of whether they're tilted. Make it binary: the trigger fires, you walk, and there is no in-the-moment decision to get wrong. Fifteen minutes, the rest of the hour, the rest of the day — the duration matters less than the rule being automatic.

- Set a session-level stop in advance.Before the session, decide the loss that ends your day — a dollar figure or a percentage — and treat it as a circuit breaker, not a suggestion. The point of setting it in advance is that the calm trader picks the number while their impulse control is intact; the tilted trader merely obeys it. Use the risk/reward calculator to think through what a normal session's R looks like, so the limit sits where a genuinely bad day stops rather than where an ordinary drawdown trips it.

- Re-enter through a checklist, not a feeling.When you do come back, the first trade after a break goes through the same setup checks as any other — planned setup, size that fits the risk, stop where the chart says it goes — and not through the urge to make the morning back. A pre-committed position size is the cleanest version of this: the number is decided once, in a calm state, so the post-tilt trader can't quietly size to the feeling. Re-entry is a checklist you pass, not a mood you wait out.

Measuring tilt

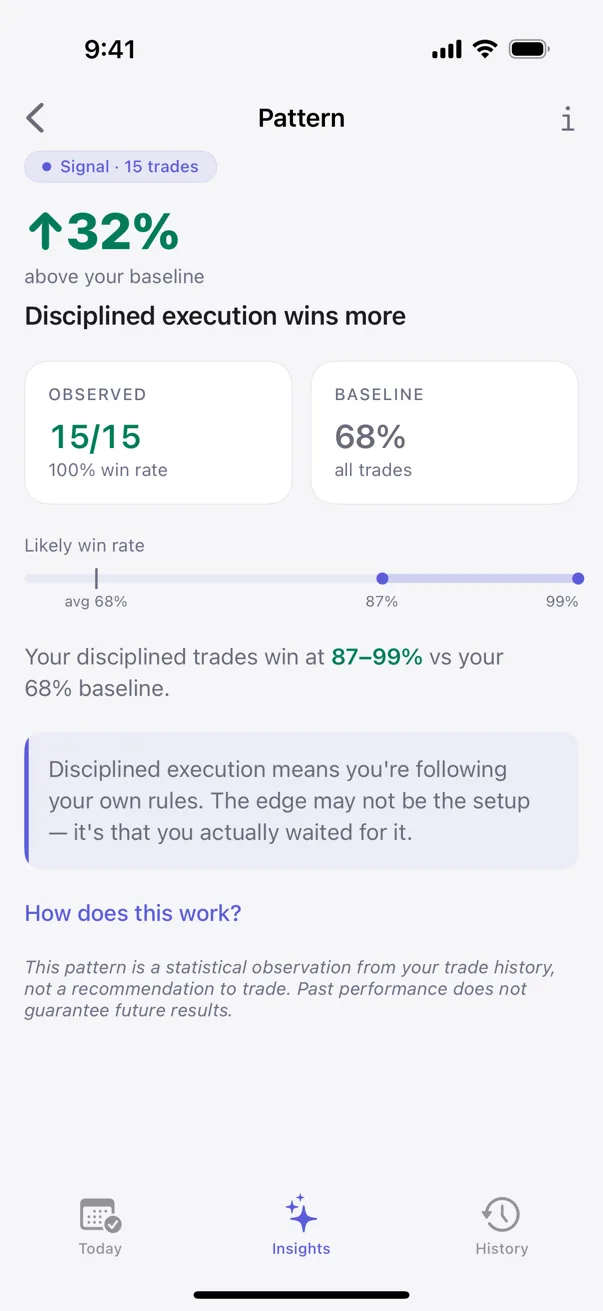

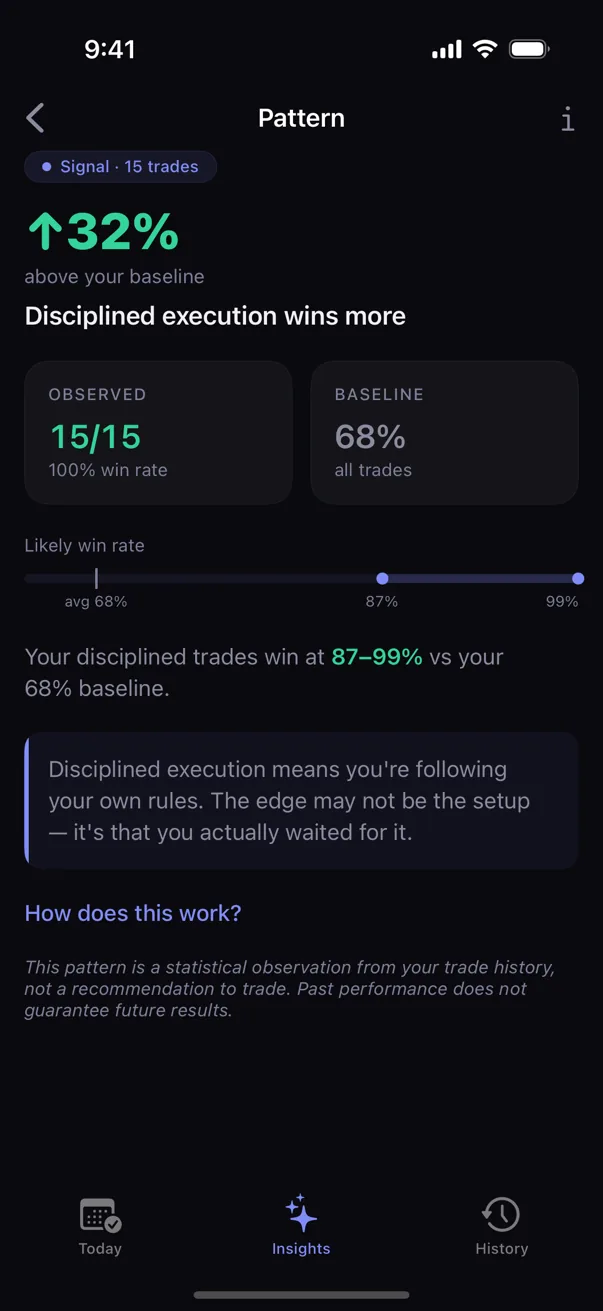

The reason tilt is hard to fix from self-narrative is the reason it's tractable from data: the state is invisible to the trader in the moment, but the run it produces is not invisible in the log. A trader can be certain they "stay disciplined after losses" and be wrong, because the calm version writing that sentence is not the version that took the trades. The trades themselves don't have that problem.

This is what behavioral pattern detection measures. Kyra detects emotional-state streaks: when a tagged state — frustrated, anxious, hyped, impulsive — coincides with worse outcomes across a run of consecutive trades, that's surfaced as a pattern with a sample size attached. The output is not a warning ("watch out for tilt"). It is a measurement: the trades you logged in a frustrated state, in runs after a loss, returned X% less than your baseline, with a confidence range that tightens as the sample grows. That number is harder to argue with than a feeling, and harder to ignore, because it's pulled from the trader's own money.

Kyra Trading is a private trading journal that does this detection on-device. The engine uses Bayesian estimation and Fisher's exact test, and labels each pattern by how much data stands behind it — Tracking, Hint, Signal, or Proven — so a streak built on six trades never reads with the same weight as one built on sixty. Every pattern surface includes the sample size and a confidence range, so the trader can see how strong the signal is. Nothing leaves the device. Pattern detection runs locally, no accounts, no servers. The trader's data stays the trader's data.

Sources

- Lo, A. W., Repin, D. V., & Steenbarger, B. N. (2005). Fear and Greed in Financial Markets: A Clinical Study of Day-Traders. American Economic Review, 95(2), 352–359.

- Coates, J. M., & Herbert, J. (2008). Endogenous steroids and financial risk taking on a London trading floor. Proceedings of the National Academy of Sciences, 105(16), 6167–6172.

- Steenbarger, B. N. (2015). Trading Psychology 2.0: From Best Practices to Best Processes. Wiley.

Educational only. Not financial or trading advice. Behavioral patterns described above are observations from the published literature; specific outcomes vary with strategy, market conditions, and individual circumstances.