What mental accounting is

Mental accounting is the set of cognitive rules people use to sort, track, and evaluate financial outcomes. Richard Thaler coined the term in 1985 [1], drawing on the same research program that produced prospect theory: the finding that people’s financial decisions deviate systematically from what a rational agent with a single, unified account balance would do. The core observation is that money is not treated as fungible. People sort it into separate mental accounts — paycheck, savings, windfall, “mad money,” profits — and apply different spending and risk rules to each, even when the dollar amounts are identical.

The mechanism is not irrational in origin. Separate mental accounts reduce cognitive overhead in ordinary life: the rent money and the discretionary money stay partitioned so every dollar does not have to be re-evaluated against every possible use. The problem in trading is that the partitioning produces asymmetric risk behavior — the “house money” account gets gambled more readily than original capital, and the break-even account reaches for recovery trades the plan would never sanction.

Unified account

Every dollar is equivalent regardless of how it was earned or classified. A $500 profit and a $500 original stake are identical inputs to the next decision.

Partitioned accounts

Profits feel different from principal. The “house money” account runs looser rules than the “real capital” account — even when both are funded from the same brokerage balance.

The house money effect in trading

Thaler and Johnson’s 1990 paper [2] documented what casinos had long relied on: after a gain, people take significantly larger risks with the winnings than they would with equivalent money drawn from their original stake. The gains sit in their own mental account, and losing them does not register as a loss of the same magnitude as losing original capital. The paper named this the “house money effect” — a gambler willing to bet wildly with chips just won from the house, because losing them only returns things to where they started.

In trading, the effect surfaces whenever a session is running profitable. The next setup gets a bigger position because “I’m up anyway.” The stop is set a little wider because “I can afford to give this one room.” A setup that would have been passed at flat P/L gets taken because the positive session balance is absorbing the perceived risk. None of those decisions are anchored to the setup’s actual edge. They are anchored to the session’s P/L, which has no bearing on what the next trade is worth.

Three behaviors it drives

Mental accounting produces three distinct distortions in trading behavior. They look like different problems in the log but share one root: risk tolerance calibrated to session state rather than to edge and volatility.

Session-state sizing

Position size drifts upward during a profitable session and shrinks after a losing one — not because setup quality changed, but because the mental accounts are stocked differently. A trader who sizes a third larger after a good first hour and a third smaller after a rough open has let the morning’s outcome set the afternoon’s risk parameters. The plan said nothing about that adjustment. The mental account did.

The “playing with profits” rationalization

A profitable run produces explicit reasoning: “I’m only risking today’s gains at this point, not my real money.” The conclusion — that looser rules apply — follows logically from the mental account framing. But the brokerage account makes no such distinction. The funds are the same. The rules that protect original capital protect profits too; a trader who would stop after losing $500 of original capital should stop at the same threshold when profits turn the loss.

The break-even push

The mirror of the house money effect: after a loss, traders take extra risk to get back to flat. Thaler and Johnson documented this alongside the house money effect — they called it “trying to break even.” The mechanism is the mental account that must be zeroed out before the session can close. A trader down $800 who sizes into a marginal setup to recover the $800 is not trading the setup; they are trading the mental account deficit. This overlaps with revenge trading but the driver is subtly different: it is an accounting compulsion, not an emotional one.

What it looks like in your log

Mental accounting leaves a specific and measurable fingerprint: position sizes and stop placement that correlate with session P/L at the time of the trade, in ways the original plan does not explain.

Size distribution by session state. When trades are grouped by the session P/L at moment of entry — profitable, flat, or negative — mental accounting produces a consistent spread: larger average sizes on profitable sessions, normal or smaller on negative ones. The variance is not explained by volatility changes or setup-quality differences. It is explained by which mental account the trader felt they were drawing from.

Stop placement by session state. A trader running mental accounting often sets wider stops on profitable sessions (“I can afford to give this room”) and tighter or more anxious ones on losing sessions. Stops sized from a plan should not vary with session P/L — their distance from entry reflects the trade’s logic, not the morning’s score.

Late-session trade frequency on losing days. The break-even push produces a characteristic pattern: trade count rises in the final hour of a losing session as the trader searches for a recovery trade. If trade frequency on down days is consistently higher than on up days in the same time window — and setup quality has not changed — the break-even mechanism is running.

Why knowing this doesn’t fix it

Mental accounting is not a logical error made from ignorance. It is a structural feature of how the human value system handles gains and losses — documented across cultures, income levels, and levels of financial sophistication. Barberis and Thaler’s survey of the behavioral finance literature [3] notes that mental accounting persists even in professional settings, because the partitioning is not a mistake so much as a feature of human cognition that misfires in financial contexts.

The implication for trading is the same as for loss aversion or recency bias: the knowledge is a label, not a lever. A trader who has read Thaler’s paper still sizes up on winning sessions, because the looser risk tolerance on the profit account is felt rather than calculated. Understanding why it happens describes the pull. It does not remove it.

Structural defenses

The defenses that work share a common design: the position size decision is made by a rule set when the trader is flat and calm, and enforced on the trader who is up $3,000 or down $1,500 and feeling the pull of the respective mental account.

- Size from equity, not session P/L.The position size calculator takes account equity and risk-per-trade percentage as inputs and returns a share count. The equity input should be the same number at the start of every session — total account balance, not “account balance minus today’s losses” or “account balance plus today’s profits.” If you find yourself entering a lower equity number to justify a smaller trade after a loss, the break-even account is speaking, not a sizing rule.

- Set daily loss limits and profit-taking pauses before the session.A daily stop-out — decided when the account is flat — removes the late-session break-even push. A symmetric rule (pause trading after a large gain, same as after a large loss) removes the house money effect’s most dangerous operating window. The pause after a gain feels unnecessary in the moment, which is precisely why it needs to be set in advance rather than evaluated when the P/L is already positive.

- Log the planned size alongside the actual size.After each trade, record the size the plan called for and the size actually taken. The correlation between actual-minus-planned size and session P/L at entry is the mental accounting signal. It is invisible trade-by-trade and legible across twenty trades in a log. Without the record, a trader who consistently oversizes on profitable sessions describes the behavior as “pressing my edge when things are working.” The log shows whether the edge changed or just the mental account.

Measuring your own mental accounting

Mental accounting is not binary. Some traders partition profits aggressively and original capital conservatively; others run a single mental account across the session; most are somewhere in between and vary with account state, recent outcome, and session length. The question is not whether the effect is present but whether it is large enough to produce a measurable cost.

Two comparisons in your trade log reveal it. First, average position size on sessions where you are in profit at moment of entry versus sessions where you are flat or negative — a gap that cannot be explained by planned size differences or volatility changes is the house money effect. Second, late-session trade frequency on negative days versus positive days — a reliable uptick on losing days, particularly in the last hour, is the break-even push.

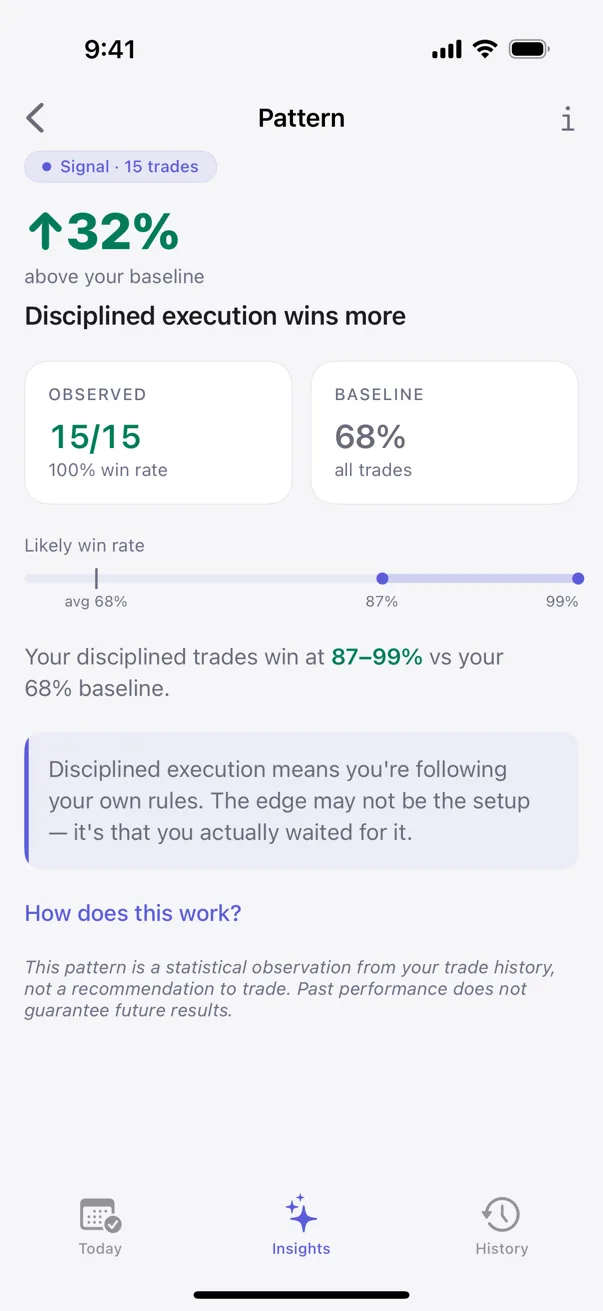

Kyra detects position-size patterns across your log, including correlations between entry size and session P/L state. When a pattern clears a minimum sample threshold it surfaces as a detected finding, tagged with a confidence tier — Tracking, Hint, Signal, or Proven — so early observations are labeled differently than confirmed ones. The pattern card shows the baseline comparison so you can see whether your sizing variance is within normal range or reflects a systematic tilt. Everything runs on-device; nothing leaves the phone.

Sources

- Thaler, R. H. (1985). Mental Accounting and Consumer Choice. Marketing Science, 4(3), 199–214.

- Thaler, R. H., & Johnson, E. J. (1990). Gambling with the House Money and Trying to Break Even: The Effects of Prior Outcomes on Risky Choice. Management Science, 36(6), 643–660.

- Barberis, N., & Thaler, R. (2003). A Survey of Behavioral Finance. In G. Constantinides, M. Harris, & R. Stulz (Eds.), Handbook of the Economics of Finance (Vol. 1, pp. 1053–1128). Elsevier.

Educational only. Not financial or trading advice. Behavioral patterns described above are observations from the published literature; specific outcomes vary with strategy, market conditions, and individual circumstances.