What FOMO trading actually is

FOMO trading is the entry that exists because someone else's profit started to look like your loss. The thesis was not yours. The setup did not appear on your watch list before the move. The decision to enter is shaped less by the chart in front of you and more by the price action that has already happened.

Three things define the sequence:

- A move that already started — the initial entry signal is in the rear-view mirror; the trade is chasing what already moved

- An external amplifier — the move is signal-boosted by social proof: a feed, a chat room, a news headline, a screenshot

- Position sized by feeling, not by risk — the size reflects "I have to be in this," not "this is what my model says I can risk on this setup"

If those three line up, the trade is not the trade you would have entered if you had spotted the move yourself. It is a trade about the feeling of having been left out.

Why it happens — three behavioral mechanisms

Calling FOMO a discipline failure misses the point. The behavioral economics and psychology literature has mapped the underlying mechanism, and "willpower" is not the lever.

Regret aversion

Regret theory [1] established that decisions under uncertainty are not driven only by expected outcomes. They are shaped by anticipated regret. A trader who watches a setup run without taking it does not feel "I missed an opportunity." They feel "I am going to regret this if it keeps going."

For the trader watching a move run, the regret of missing it is vivid and immediate, while the risk of a chased loser is abstract and deferred. So the trader enters, not to capture the trade, but to neutralize the anticipated regret of missing it. The math of the trade is secondary. The math of the felt loss is what is being optimized.

Informational cascades

Bikhchandani, Hirshleifer, and Welch's foundational paper on cascades [2] showed that rational individuals will rationally ignore their own private information once enough other actors appear to be acting on contrary information. In trading, this looks like: your model says wait. Price is moving with conviction. A feed of voices says "in." Private signal says wait, cascade signal says go.

The cascade is not always wrong. Sometimes the move is real. But cascade entries are characteristically the worst-priced entries in a move, because they happen after the information has already been priced in by the actors at the front of the cascade. The trader at the back pays the most for the same conviction.

Attentional narrowing under arousal

Easterbrook's classical work on cue utilization [3] showed that elevated arousal narrows the range of cues a person attends to. A FOMO entry happens at exactly the moment of peak arousal: the chart is moving fast, the feed is loud, the trader is running on adrenaline. In that state the cues a careful trader would normally check (R-multiple, position-sizing rule, daily loss limit, time-of-day discipline) are not absent. They are out of frame.

This is why FOMO trades are systematically poorly sized. The trader is not ignoring sizing. The sizing cue is simply not in the narrow band of information their attention can reach right now.

The fingerprint in your trade log

FOMO trades have a fingerprint. They look like this:

- Entry timestamp clusters around social-signal events: large green-candle prints, news headlines, viral posts

- Entry price is well above the most recent meaningful pivot — the entry is multiple ATRs into the move, not at the start of it

- Position size is at or above the trader's average, often larger than their stated rule allows

- The risk/reward on the planned exit is poor — the room left to the logical target is small relative to the room down to a sensible stop

- The setup tag (if used) does not match how the trader normally categorizes that asset

- Exit plan is vague or absent: the entry was not paired with a deliberate exit decision

- The reflection field, when filled in honestly later, contains the words "should have," "was up," or "kept going"

This is not a hypothetical. It is the structure that pattern detection picks up. The "emotion = FOMO" pattern is one of the cleanest signals in retail trading data, because the entry sizing and ATR-extension at entry are diagnostic on their own.

Three structural defenses

These work because they do not require the moment-of-FOMO trader to be disciplined. They require the calm trader to set up rules that the moment-of-FOMO trader will run into.

1. The named-watchlist rule

Only enter trades on instruments named on your watch list before the session began. The watch list is set in calm. It cannot be amended during the session. If a name is not on the list, it is not a trade today, regardless of how loudly the move is happening.

This works because it removes the question. The FOMO trader is not deciding whether to enter; they are checking whether the name is on a list, and lists do not negotiate.

2. Pre-defined position size

Before market open, decide your position size for every potential trade today. Write it down. Use a position size calculator to lock in a number that does not depend on how the morning goes.

FOMO trades are characteristically oversized. The defense is to remove sizing from the moment of entry. The post-FOMO trader cannot be trusted to size; the pre-market trader can. The number on paper is how the calm trader makes the FOMO trader obey.

3. The 5-minute setup-validity check

If you find yourself wanting to enter a trade you did not plan to take, set a 5-minute timer before clicking the button. During those five minutes, ask one question: is the setup that prompted this still valid right now, or has the move already happened?

Use the risk/reward calculator to confirm the math: a chase entry near the top of a move usually has the worst R-multiple of any entry in the cycle. Most FOMO entries fail this check. The setup the trader is reaching for ran twenty minutes ago. Current price is the price after the setup completed.

The mechanism is the same as the post-loss pause that interrupts revenge trading: the moment-of-trade decision-maker is impaired; give them time to refresh.

Why most advice does not work

The internet is full of "do not chase trades" advice. Trading psychology books are full of it. Most of it is correct. Almost none of it is useful in the moment.

The reason: the advice assumes the trader can interrupt their own behavior in real time. The mechanism above suggests they cannot, at least not without scaffolding. The moment-of-FOMO trader is operating with narrowed attention, anticipated-regret pressure, and cascade-driven conviction. Asking the impaired person to override their impairment is asking the wrong person.

What works is structural. Watch lists set in advance. Sizing rules locked before market open. Process journaling that catches the sequence after the fact and surfaces it before it becomes habit.

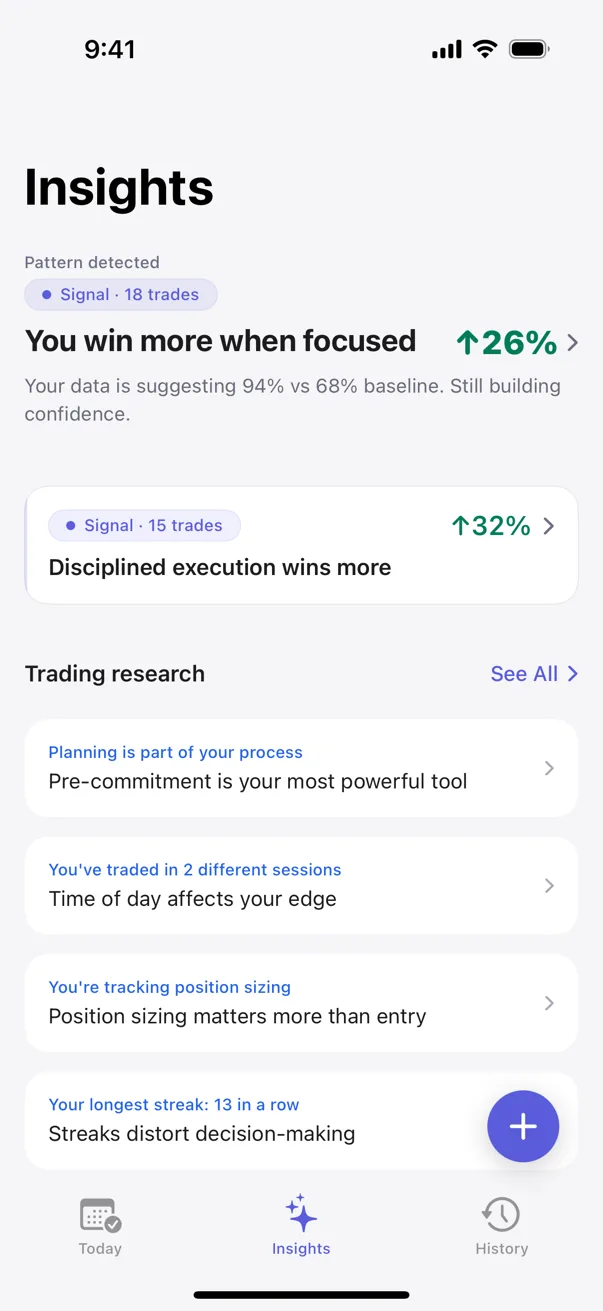

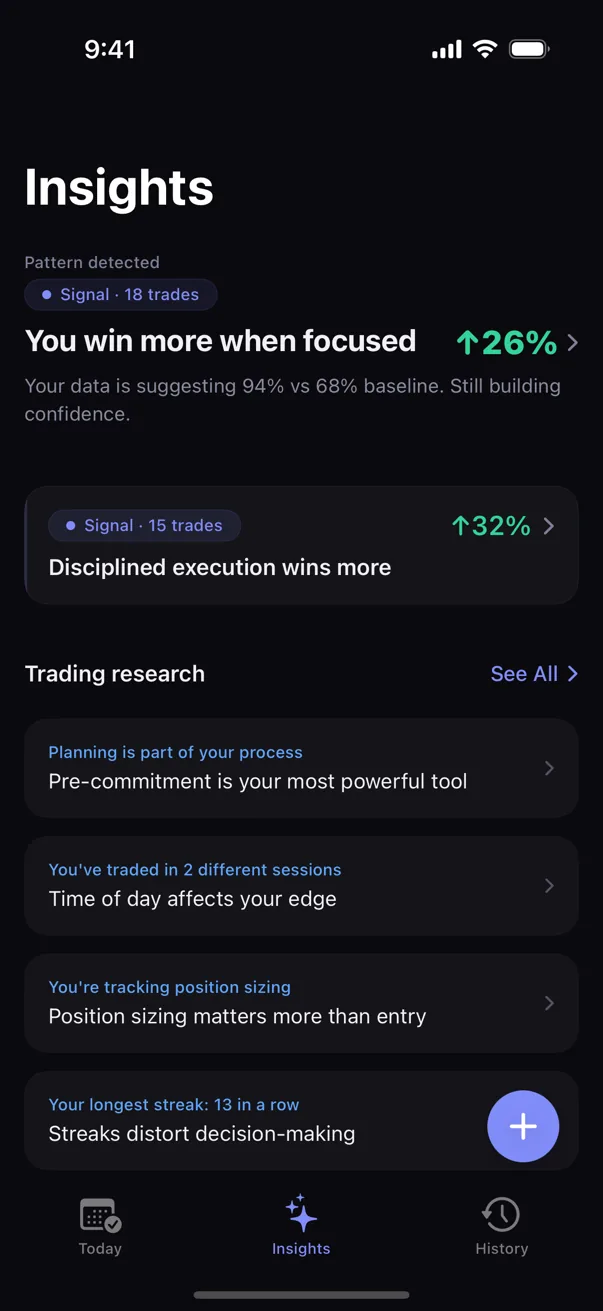

The measurement layer

Behavioral pattern detection — running statistical tests across a trader's own trade history — closes that gap. The output is not a warning ("watch out for FOMO"). It is a measurement: the trades you tagged FOMO in the last 90 days returned X% less per trade than your baseline, with a confidence range from [low] to [high]. That number is harder to argue with than a generic warning.

Kyra Trading is a private trading journal that does this detection on-device. Every pattern surface includes the sample size and a confidence range, so the trader can see how strong the signal is. Nothing leaves the device. Pattern detection runs locally, no accounts, no servers. The trader's data stays the trader's data.

Sources

- Loomes, G., & Sugden, R. (1982). Regret Theory: An Alternative Theory of Rational Choice Under Uncertainty. The Economic Journal, 92(368), 805–824.

- Bikhchandani, S., Hirshleifer, D., & Welch, I. (1992). A Theory of Fads, Fashion, Custom, and Cultural Change as Informational Cascades. Journal of Political Economy, 100(5), 992–1026.

- Easterbrook, J. A. (1959). The effect of emotion on cue utilization and the organization of behavior. Psychological Review, 66(3), 183–201.

Educational only. Not financial or trading advice. Behavioral patterns described above are observations from the published literature; specific outcomes vary with strategy, market conditions, and individual circumstances.