What hindsight bias actually is

Hindsight bias is the tendency, once an outcome is known, to overestimate how predictable that outcome was beforehand — and to misremember your own prior judgment as closer to what actually happened. It is the "knew-it-all-along" effect: the result arrives, and your memory quietly edits the version of you that existed before it, until that earlier self appears to have seen it coming.

The effect was first measured systematically by Fischhoff in 1975. Subjects who were told an event's outcome rated that outcome as having been more likely all along than subjects who were never told — and, critically, they were largely unaware that the outcome knowledge had shifted their judgment at all [1]. The distortion is not a conscious rationalization you could choose to stop. It operates on the memory itself, below the level you can introspect.

Researchers since have separated the effect into distinct components: a memory distortion (mis-recalling your earlier prediction), an inevitability belief (the outcome "had to" happen), and a foreseeability belief (you personally could have known) [3]. All three converge on the same result for a trader: the gap between what you actually decided and what happened gets erased, and with it the only information a review exists to recover.

The trade, before the outcome

Your real thesis, your planned exit, the size you intended, the state you were in. Uncertain, incomplete, made without knowing the result — the actual decision under review.

The trade, after the outcome

Re-narrated by the result. The win looks intentional, the loss looks foreseeable, and the messy uncertainty that was actually present has been smoothed away. The version you review instead.

Why the rewrite feels like the truth

The reason hindsight bias is so durable is that the edited memory does not feel edited. It feels like recall. When you look back at a losing trade and think "I knew that breakout was weak," there is no internal signal distinguishing a genuine prior doubt from one the loss installed retroactively. The confidence attached to the false memory is the same confidence that attaches to a true one.

Markets make this worse than most domains because outcomes are noisy. A sound decision can lose and a reckless one can win, so the result is a weak signal about the quality of the choice. Hindsight bias takes that weak signal and treats it as a verdict — it lets the outcome stand in for the analysis of the decision, which is a related error sometimes called outcome bias. The trade that worked gets filed as a good decision regardless of whether the reasoning held; the trade that failed gets filed as an obvious mistake regardless of whether it was well-judged at the time.

There is a measured cost to this. Biais and Weber studied hindsight bias in a financial setting and found that subjects more prone to it formed less accurate assessments of risk and, consequently, earned lower investment returns — because a trader who believes outcomes were foreseeable underestimates volatility and learns the wrong lessons from experience [2]. The bias does not just distort the story; it degrades the next decision.

What it looks like in practice

Hindsight bias tends to surface in three places, and all of them sit inside the review process where traders go to improve.

The first is the loss post-mortem. You replay a losing trade and arrive quickly at "I should have seen it" — the reversal candle, the weak volume, the news that dropped. The certainty feels like insight, but it is often the outcome painting the chart backward. The lesson you take away ("watch for that reversal") is built on a pattern that was not actually legible in real time, so it does not generalize, and the real lesson — that the entry was sound and the variance was normal — never lands.

The second is the win audit, where the bias is more flattering and more dangerous. A trade that worked gets remembered as a deliberate read, even if the exit was luck and the entry barely passed your screen. Crediting yourself with judgment you did not exercise inflates your estimate of your own skill, which is the input to your next sizing and selection decision. Skill assessment built on hindsight-edited wins runs ahead of the real edge.

The third is the abandoned plan. Because hindsight collapses the distinction between what you planned and what happened, a trader stops being able to tell whether a trade followed the plan or just happened to end well. Over time the plan itself loses authority — why follow a checklist when memory says you "just knew" the right move each time? — and discretion creeps back in under the cover of remembered competence.

The fingerprint in your trade log

Hindsight bias has one structural weakness: it can only rewrite memory, not a record made before the outcome was known. The fingerprint, therefore, is not in any single number — it is in the gap between what you committed to in advance and what you later believe you did. A log that captures intent before the result exposes that gap; one reconstructed afterward simply inherits the bias.

- Stated thesis vs remembered thesis. If you record why you are entering before the trade resolves, you can check it against the story you tell in review. When the post-trade narrative ("I was worried about resistance") has no match in the pre-trade note, that is hindsight writing fiction.

- Planned exit vs claimed intention. A logged exit target, set at entry, settles whether a profitable exit was the plan or a lucky stumble you have since promoted to strategy.

- Decision quality vs outcome. Tagging whether a trade followed your rules — independent of whether it won — lets you separate process from result. If your "good decisions" correlate perfectly with your winners, outcome knowledge is doing the grading, not your rules.

- Lessons that never change behavior. A review that produces a fresh "obvious" lesson after every loss, none of which alters the next trade, is a review running on hindsight rather than evidence.

How to counter it

Write the thesis before the outcome exists

The single most effective defense is a contemporaneous record: capture your reasoning, your planned exit, and your intended size at entry, while the result is still unknown. A note written before the trade resolves cannot be edited by the outcome, because the outcome had not happened yet. This is the one piece of evidence hindsight bias cannot reach — and it is worthless if reconstructed later from memory, so it has to be made in the moment.

Grade the decision, not the result

In review, judge each trade on whether it followed your process — the setup was valid, the risk was defined, the entry matched the plan — separately from whether it made money. A well-executed trade that lost to variance is a good decision; a rule-breaking trade that won is a bad decision that paid. Holding those two axes apart is what stops the outcome from grading the choice, and it is impossible to do without a record of what the choice actually was.

Review against the record, not the recollection

When you sit down to learn from a trade, read the pre-trade note first, before you let yourself narrate. Anchor the review to what you wrote, then compare it to what happened. The lessons that survive that comparison — a setup that genuinely underperforms, a state that genuinely precedes losses — are real. The ones that only appear when you reason backward from the outcome are hindsight, and acting on them adds noise.

The measurement layer

Countering hindsight bias depends on having a record made before the outcome, and on being able to compare it to what actually happened without your memory in the loop. That is a measurement problem, and it is the part a journal can carry that willpower cannot.

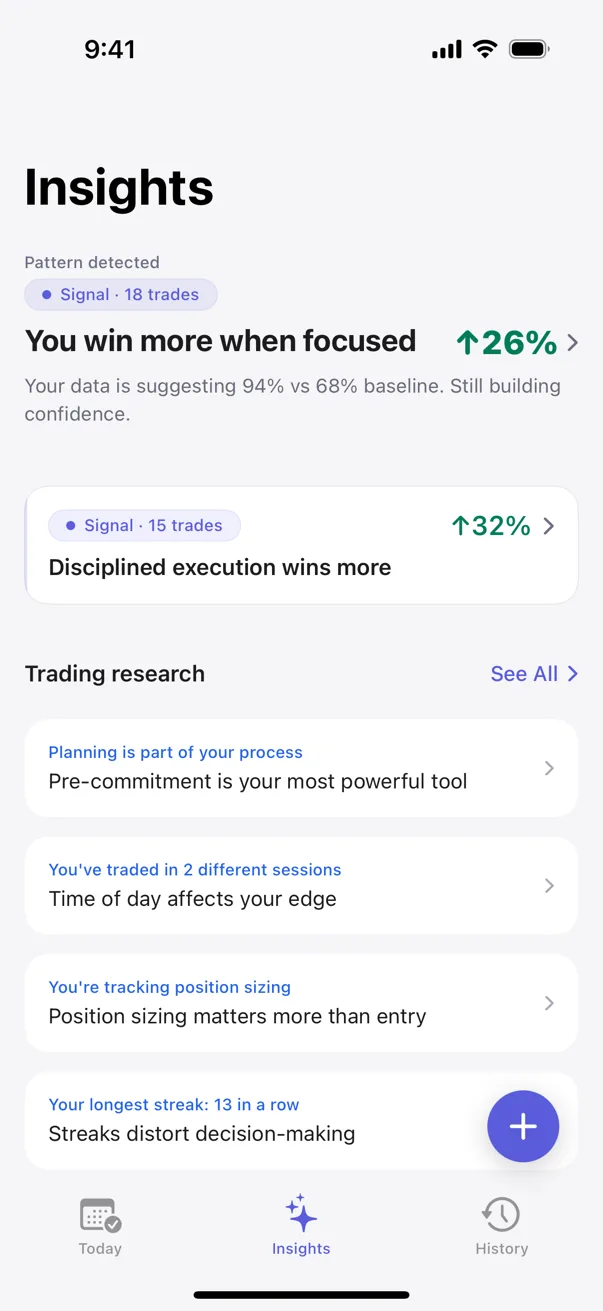

Kyra Trading's pre-trade checklist captures your intent before the trade is live — whether it was a planned setup, whether you had a defined stop and an exit target, the size you meant to take, and the emotional state you logged in the moment. Because that record predates the result, your later review has something fixed to check against: the trade you actually set up, not the one the outcome rewrote.

Pattern detection then runs across what was logged, not what is remembered. The analysis covers your full history of recorded trades and decisions, and the confidence tiers — Tracking, Hint, Signal, Proven — reflect how much real evidence sits behind a finding before it surfaces. A lesson that feels obvious after one loss stays in Tracking until the data actually supports it; a pattern with Proven status behind it is built on the record, not on a story the last outcome installed. The gap between your stated plan and your outcomes becomes a number you can see, instead of a memory you can edit.

Kyra runs all detection on-device. Nothing leaves your phone — no accounts, no servers, no shared data. The record stays private, and it stays honest because it was written down before you knew how it ended.

Sources

- Fischhoff, B. (1975). Hindsight ≠ foresight: The effect of outcome knowledge on judgment under uncertainty. Journal of Experimental Psychology: Human Perception and Performance, 1(3), 288–299.

- Biais, B., & Weber, M. (2009). Hindsight Bias, Risk Perception, and Investment Performance. Management Science, 55(6), 1018–1029.

- Roese, N. J., & Vohs, K. D. (2012). Hindsight Bias. Perspectives on Psychological Science, 7(5), 411–426.

Educational only. Not financial or trading advice. Behavioral patterns described above are observations from the published literature; specific outcomes vary with strategy, market conditions, and individual circumstances.