What confirmation bias actually is

Confirmation bias is the tendency to search for, interpret, and recall information in a way that confirms what you already believe. Raymond Nickerson, in a comprehensive 1998 review of the psychological literature, described it as “a ubiquitous phenomenon in many guises” — one of the most consistent findings in all of cognitive psychology [1].

In trading, the belief at stake is your open position. The moment you enter, you hold a view — this instrument, this direction, this timing. Every piece of information that arrives after that point is filtered through it. The filter does not announce itself. It operates quietly, at the level of what you notice, what you weight, and what you explain away.

Confirming evidence

Price action moving in your direction. News or commentary that supports the thesis. Technical signals that align with the entry. Other traders expressing the same view.

Contrary evidence

Price stalling or reversing before the target. Volume that does not confirm the move. Data that contradicts the thesis. Your stop getting close without a re-evaluation.

Why it happens

The brain is a prediction engine, not a truth machine. Once it commits to a hypothesis, it becomes efficient at locating supporting evidence — and metabolically costly to reverse course. That asymmetry was useful over most of human history, where fast commitment beat accurate updating. In a market, where the cost of the wrong prediction is real and measurable, the same asymmetry produces systematic error.

Lord, Ross, and Lepper demonstrated this in a 1979 study on attitude polarization. Participants shown the same mixed evidence on a contested topic consistently rated studies that confirmed their prior view as more methodologically sound than studies that challenged it — even when the two studies were identical in design [2]. Same data; different verdicts. The only thing that decided the rating was whether the result matched what the participant already believed.

In trading, entry is the moment you form a belief. Every tick after that is filtered through it.

The evidence

Kahneman and Tversky's foundational work on representativeness and prediction showed that people systematically overweight information that matches their mental model of what a good outcome looks like, and underweight base rates — the statistical background that should anchor any forecast [3]. A setup that “looks like” prior winners attracts more conviction than the actual historical success rate of that setup warrants. The match to a template substitutes for the evidence.

This is why high-conviction trades are the most difficult ones to analyze honestly. The stronger the prior belief, the more aggressively the brain suppresses information that challenges it. Conviction and accuracy are not the same thing — and in the presence of confirmation bias, they can move in opposite directions.

The fingerprint in your trade log

Confirmation bias does not label itself. But it leaves consistent patterns in the data:

- Stop widening on adverse price action. The stop moved because the trade “needs room” — and the move coincided with price approaching that stop, not with a genuine re-evaluation of the setup. The thesis did not change. The stop moved because closing would have meant admitting the trade was wrong.

- High-conviction asymmetry. Trades rated as high-conviction show lower plan-adherence than your average trades. When the prior belief is strongest, the rules get bent most.

- Rules cited at entry, not enforced at exit. The entry note references the setup criteria clearly. The exit note, when price moved against you, is brief or absent. The position stayed open past the invalidation point without a recorded reason why.

- Extended holding on losing trades. Positions that are down stay open longer than the plan called for, with each passing session producing a new reason the thesis might still resolve.

How to counter it

Write the invalidation before entry

Before the trade runs, complete this sentence: “I will exit this position if ___.” Not a loss level — a condition. What would have to be true in the market for your thesis to be wrong? Name the condition explicitly and record it with the entry note. A condition named in advance is much harder to explain away in real time than one constructed after the fact.

Seek the contrary case before adding or widening

Before increasing a position size or widening a stop, find the strongest argument against the trade. Not a weak objection — the actual best case for why you are wrong. If you cannot construct it, you have not understood the other side of the market. If you can construct it and it is compelling, that is information worth acting on.

Audit your high-conviction trades separately

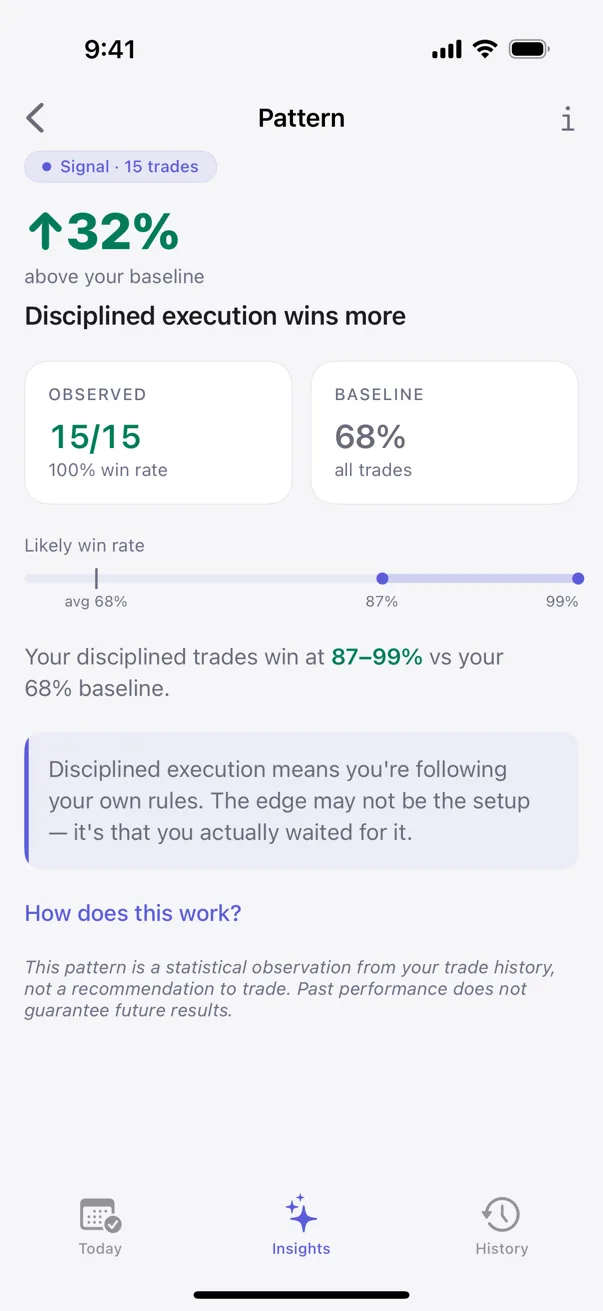

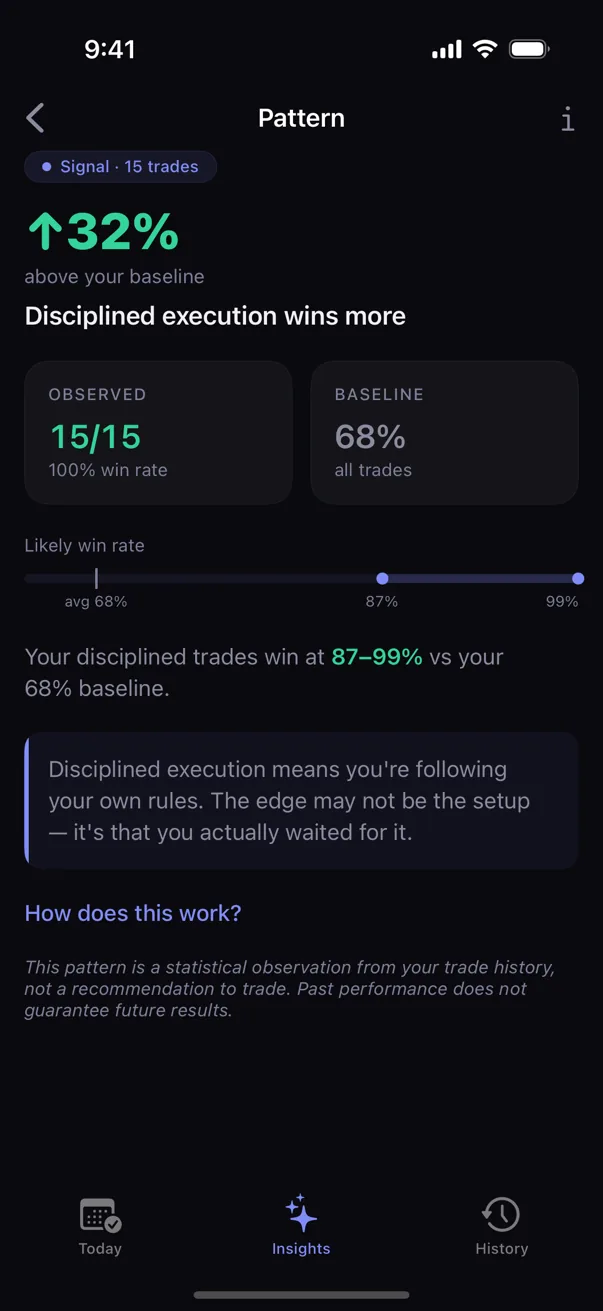

Pull the subset of trades you rated at maximum conviction. Compare stop-adherence, exit-plan adherence, and outcome distribution against your full population. If your highest-conviction trades show worse discipline — or underperform the average — conviction is amplifying bias, not improving decisions. Most traders do not know which it is. The sample tells you.

The measurement layer

Knowing about confirmation bias does not tell you whether you have it, or how much it costs you. The research describes populations, not individuals. And self-report is particularly unreliable here — the trader sitting in a biased position is also the one who would describe themselves as evaluating it objectively.

Kyra captures conviction rating at entry as a standard field. After a sufficient sample builds, the pattern becomes visible: do your high-conviction entries hold to the exit plan at a higher rate, or a lower one? Do they reach the stated target more often than your average, or less? The answer is in the log. It is not available from memory or intuition.

Sources

- Nickerson, R.S. (1998). Confirmation bias: A ubiquitous phenomenon in many guises. Psychological Review, 105(2), 211–233.

- Lord, C.G., Ross, L., & Lepper, M.R. (1979). Biased assimilation and attitude polarization: The effects of prior theories on subsequently considered evidence. Journal of Personality and Social Psychology, 37(11), 2098–2109.

- Kahneman, D., & Tversky, A. (1973). On the psychology of prediction. Psychological Review, 80(4), 237–251.

Educational only. Not financial or trading advice. Behavioral patterns described above are observations from the published literature; specific outcomes vary with strategy, market conditions, and individual circumstances.