What the disposition effect actually is

The disposition effect is an asymmetry at the exit. Faced with a position that is up, the trader tends to close it — to bank the gain. Faced with a position that is down, the same trader tends to hold — to wait for it to come back. Same trader, same account, opposite reflex, and the only thing that decides which reflex fires is whether the position is currently green or red.

The name comes from Hersh Shefrin and Meir Statman, who in 1985 gave the pattern its label and first formal treatment: "the disposition to sell winners too early and ride losers too long" [1]. The phrase is precise. It is not "sells winners" or "holds losers" in isolation — plenty of strategies do one or the other on purpose. It is the pairing: a systematically lower bar for realizing a gain than for realizing a loss, applied to the same book by the same person.

The tell is that the decision is being made on the position's color rather than on its thesis. A disciplined exit asks whether the reason for the trade still holds. A disposition-driven exit asks whether the position is up or down — and lets that answer decide.

The quick exit

Closed early to lock in the gain. The win feels secured the moment it's realized, so the bar to sell is low — even when the move has room left and the thesis is intact.

The held loser

Kept open to avoid realizing the loss. Selling means admitting the trade failed, so the bar to sell is high — the position rides past the plan "until it comes back."

Why it happens

The disposition effect is not a discipline failure so much as a predictable consequence of how people weigh gains against losses. The mechanism traces back to prospect theory, the framework Daniel Kahneman and Amos Tversky built to describe how real decisions under risk depart from the textbook expected-value model [3].

Two features of that framework do the work. The first is that value is felt relative to a reference point — usually the entry price — not in absolute terms. A position is not "worth $X"; it is "up $200" or "down $200" from where you got in. That reference point is what splits every open trade into a winner or a loser in the first place.

The second is loss aversion: a loss of a given size hurts more than a gain of the same size pleases. Realizing a gain is a clean, pleasant act — it converts a paper win into a booked one and closes the chapter on a high note. Realizing a loss is the opposite: it makes the paper loss permanent and admits, on the record, that the trade was wrong. Because the second act is the more painful one, the trader avoids it — and the avoidance looks, from the outside, exactly like "holding losers until they come back."

This is why the asymmetry is so durable. The trader is not choosing to be inconsistent; each individual exit feels locally reasonable. Banking a win feels prudent. Giving a loser "a bit more room" feels patient. It is only when the two reflexes are viewed side by side, across many trades, that the systematic tilt becomes visible.

The evidence

The disposition effect is not a tidy theory in search of data. It is one of the most directly measured biases in behavioral finance, and the cleanest measurement is Terrance Odean's 1998 study of trading records from a large discount brokerage [2]. Odean built a direct test: for every sale, he compared the gains a trader actually realized against the gains they could have realized but didn't, and likewise for losses. The result was a sharp asymmetry — individual investors realized their gains at a markedly higher rate than their losses. Winners were far more likely to be sold; losers were far more likely to be kept.

The second half of the finding is what makes the behavior costly rather than merely irrational. Odean tracked what happened after the exits. The winners that investors sold went on, on average, to outperform the losers they held onto. So the disposition effect does not just reshuffle the timing of exits — it cuts the wrong positions. Traders were systematically closing the trades that would have kept working and clinging to the ones that kept bleeding. The bias has a price tag, and the price is paid in forgone return.

Notice that the figure is built entirely from things already in a trade log — entry timestamps, exit timestamps, and outcomes. No qualitative note is required. The gap between how long winners are held and how long losers are held is visible from the numbers alone, which is exactly why it can be detected.

The fingerprint in your trade log

The disposition effect has one of the most legible fingerprints in a trade log, because the two halves of the bias each leave a numeric trace.

- Hold-time asymmetry. Winners are closed quickly; losers are held long. Bin your trades by outcome and look at average time-in-trade — if winners exit in hours and losers linger for days, the asymmetry is there in the timestamps.

- Size asymmetry at the exit. Realized winners are small; realized losses are large. The quick exit caps the upside before it can run, while the held loser is allowed to drift well past where the plan said to cut it.

- Exits decided by color, not thesis. The pattern shows up as wins taken near the entry and losses left to run past the stop — a stop that was either widened in the moment or never enforced.

The diagnostic is the pairing. Either half alone can be a deliberate choice; together, applied to the same book, they are the disposition effect's signature. And because the signature lives in timestamps and outcomes — both already recorded — it does not depend on the trader remembering how any single exit felt.

How to counter it

The fixes that work all share a shape: they move the exit decision out of the moment, where the bias fires, and back to before the trade, where it doesn't. The exit is precisely where color overrides thesis, so the cure is to commit to both exits before there is any color to react to.

1. Decide both exits before entry

Before you enter, define the stop and the target. Not one or the other — both. The disposition effect lives in the gap between "I'll cut it somewhere down here" and "I'll let this one breathe," and that gap only exists because the exits were left open. Writing down both numbers closes it. The stop commits you to realizing a loss at a level chosen while you were calm; the target commits you to letting a winner run to a level chosen the same way.

2. Let rules govern the exit, not discretion

Discretion at the exit is where the bias does its work, because the in-the-moment trader is the one weighing a painful loss-realization against an easy gain-realization. A rule removes that weighing. "Exit at the stop, exit at the target, no renegotiation" is binary — either price hit the level or it didn't — and there is no judgment call left for loss aversion to bend. The point is not that discretion is always wrong; it is that the exit is the single worst place to spend it.

3. Size the loss before you take the trade

Half the disposition effect is letting losers grow. Capping that starts before entry, by deciding how much the trade is allowed to lose and where the stop has to sit to honor it. A position size calculator turns that into a fixed number, and a risk/reward calculator checks that the target you committed to is actually worth the stop you set — so the winner you let run is sized to matter, and the loser you cut is sized to survive. A trade whose loss is bounded in advance cannot become the held loser the bias wants it to be.

The measurement layer

Knowing about the disposition effect is not the same as knowing whether you have it, or how badly. Odean's findings are aggregate; they describe a cohort, not you. And self-narrative is a poor guide at the exit — "I cut my losers" is exactly what the trader holding a loser believes, right up until the timestamps say otherwise.

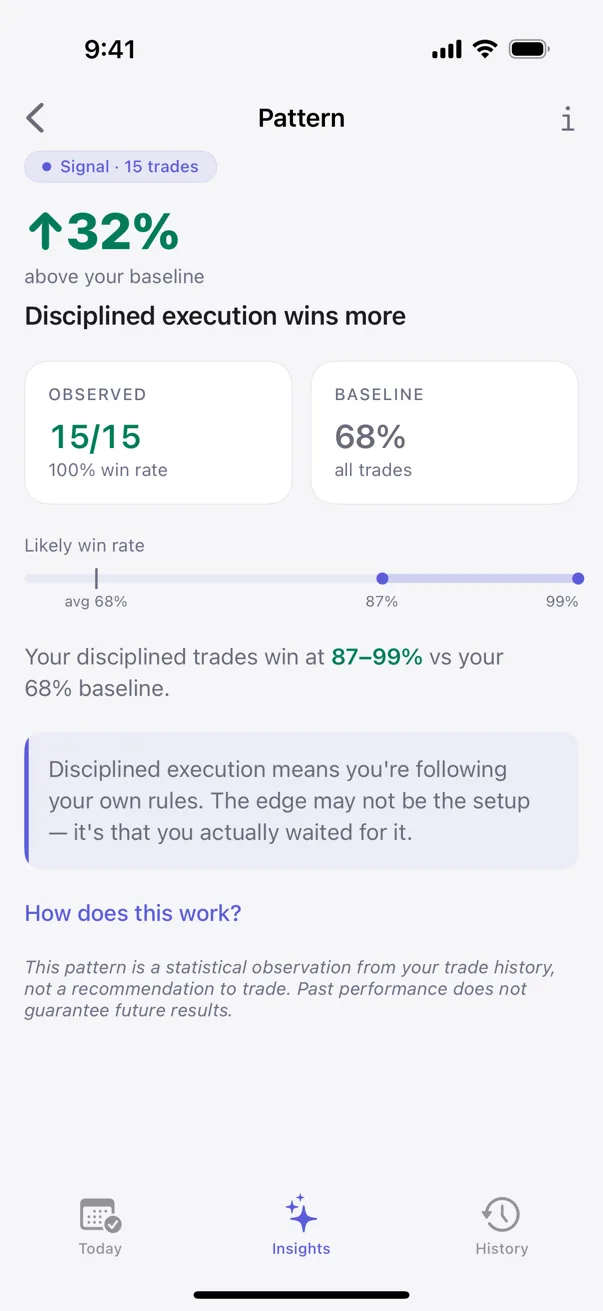

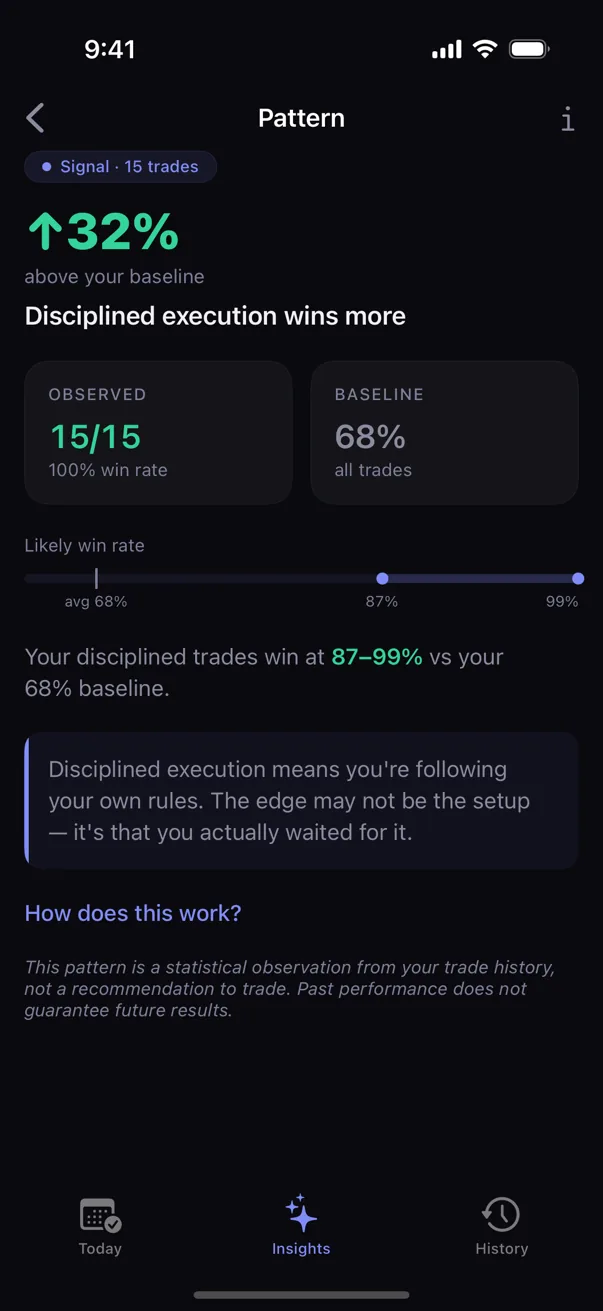

Behavioral pattern detection closes that gap by comparing hold times and outcomes for your winners against your losers and surfacing the asymmetry directly. The output is not a warning ("watch out for the disposition effect"). It is a measurement: your winners were held N hours and your losers M days, across a sample of X trades. A number pulled from your own exits is harder to argue with than a generic caution.

Kyra Trading is a private trading journal that does this detection on-device. It uses Bayesian inference and Fisher's exact test to separate a real exit-behavior asymmetry from noise, and every pattern surface carries its sample size and a confidence range, so the trader can see how strong the signal is — patterns move through Tracking, Hint, Signal, and Proven tiers as the evidence accumulates. Nothing leaves the device. Pattern detection runs locally, no accounts, no servers. The trader's data stays the trader's data.

Sources

- Shefrin, H., & Statman, M. (1985). The Disposition to Sell Winners Too Early and Ride Losers Too Long: Theory and Evidence. The Journal of Finance, 40(3), 777–790.

- Odean, T. (1998). Are Investors Reluctant to Realize Their Losses? The Journal of Finance, 53(5), 1775–1798.

- Kahneman, D., & Tversky, A. (1979). Prospect Theory: An Analysis of Decision under Risk. Econometrica, 47(2), 263–291.

Educational only. Not financial or trading advice. Behavioral patterns described above are observations from the published literature; specific outcomes vary with strategy, market conditions, and individual circumstances.