What anchoring bias actually is

Anchoring is the tendency to give disproportionate weight to the first number encountered when making a subsequent judgment. Tversky and Kahneman identified the mechanism in 1974, describing it as one of three core heuristics through which people make numerical estimates: an initial value is set, and all adjustments from that anchor are systematically insufficient [1].

In trading, anchors appear everywhere. Your entry price is the most pervasive — the moment you open a position, that number becomes a reference against which all subsequent price action is measured. Round numbers are anchors. The prior day's close is an anchor. The 52-week high and low are anchors. Any number that has been prominent in your recent attention can distort the judgments that follow it.

Holding decisions

Refusing to exit a losing position because it has not returned to entry price. Extending a stated target from $97 to $100 because a round number feels more natural. Averaging down to “lower the cost basis” rather than evaluating the position at its current price.

Entry decisions

Hesitating on a valid setup because price has moved far from the prior high. Waiting for a pullback to a round number before entering when the plan does not require it. Judging whether an instrument is “expensive” by comparing it to a remembered price level rather than the setup's own merit.

Why it happens

Tversky and Kahneman's original formulation described anchoring-and-adjustment as a two-step process: people start from an available number and adjust toward what seems like a correct answer. The key finding was that the adjustment is almost always insufficient. The anchor exerts a gravitational pull; the final estimate lands closer to the starting point than the evidence warrants.

The mechanism is partly attentional and partly computational. When your entry price is visible on a screen, it is constantly in your attentional field. Every time you evaluate the position, you start from that number. The brain does not spontaneously reset to current price and ask “given where this is now, is it the best use of capital?” It asks “how far is it from where I bought it?” — which is a different question with a different answer.

What makes anchoring particularly costly in trading is that it substitutes a reference point that is personally meaningful — where you entered — for one that is analytically relevant: where the trade stands relative to the plan. The entry price is not part of the trade's future. It is only part of your past.

The evidence

The magnitude of anchoring is larger than most people expect. Northcraft and Neale studied professional real estate agents estimating property values and found that the listing price — a number the agents explicitly acknowledged should not influence their estimate — nonetheless shifted their valuations significantly. Agents who saw a high listing price gave substantially higher estimates than those who saw a lower one, even when all other property information was held constant [2]. The agents were domain experts, aware of the potential influence, and anchored anyway.

The same effect extends into financial markets. George and Hwang documented that the 52-week high functions as a significant reference point for investors evaluating stocks: prices near the 52-week high are systematically underweighted by analysts and show predictable subsequent momentum, because the anchor suppresses buying decisions at levels that feel “expensive” relative to the recent range [3]. The 52-week high has no intrinsic relevance to any individual setup — but it shapes behavior at scale.

Both findings carry the same implication: proximity to a salient reference point alters decisions, even among people who have professional reasons to resist it.

The fingerprint in your trade log

Anchoring leaves specific, measurable patterns in trade data:

- Entry-price holding on losers. The position is held past the original invalidation point, with the exit delayed until price returns to or near the entry. The original stop — set when the trade was planned — was moved, widened, or not acted on. The reason recorded, if any, references getting back to even rather than a new assessment of the setup.

- Round-number clustering at exits. Targets and stops cluster at $50, $100, $200, or whatever round numbers are in range. When you audit whether stated targets match what was in the plan, the two often diverge: the plan said $97, the execution waited for $100. The round number was not part of the strategy — it was an anchor in the price landscape.

- Averaging down without a re-entry rationale. Adding to a losing position to lower the cost basis is anchoring made operational: the decision to average is driven by the entry price, not by a new setup. The blended cost basis after averaging is itself a new anchor, often used to defer the same exit decision.

- Hesitation near prior extremes. Setups that trigger at or near a prior significant level — a 52-week high, a round number, a prior support turned resistance — receive smaller size, delayed entries, or are skipped, not because the setup criteria changed but because the price “feels high” or “feels low” relative to a remembered level.

How to counter it

Define exits relative to market structure, not to entry

A stop set as “below the prior candle's low” or “at the point where the setup is invalidated by volatility” is derived from the trade's own logic. A stop set as “1.5% below entry” is derived from the entry price — which is an anchor. The second approach imports that anchor into the risk management. Setting exits in terms of structure or volatility removes the entry from the calculation.

Write the exit plan before you know the fill

Write your target and stop conditions before you enter the trade — ideally before you see the exact execution price. Once the fill is confirmed, the number becomes an anchor for any further planning. A plan written against “around $47” is less distorted than one written after seeing a fill at $47.83, because the precise fill price cannot pull the plan toward itself.

Audit round-number clustering in your exit data

Pull closed trade exit prices from a meaningful sample. Look at where stops and targets actually triggered. Do they cluster at $50, $100, $25? Compare those levels to what the original plan documented. If the plan said $97 and exits arrived at $100, that gap is worth examining — not because $100 is always wrong, but because it appearing systematically in ways that diverge from plans is the signature of anchoring rather than strategy.

Re-evaluate open positions at current price

For any open position, apply this check: if you did not currently hold this trade and were evaluating it as a potential new entry today, would you enter it? If the answer is no, the reason you are still in it is not a trade rationale — it is an anchor to a prior price. This is not a rule that selling is always correct; it is a test that removes entry price from the evaluation and replaces it with current structure.

The measurement layer

Knowing about anchoring does not reveal whether it is affecting your decisions or what it is costing you. The research describes a population tendency; your log contains your individual data. Self-report is unreliable here for the same reason it is unreliable in all anchored decisions: the trader assessing whether they are anchored to their entry is using that entry price to do the assessment.

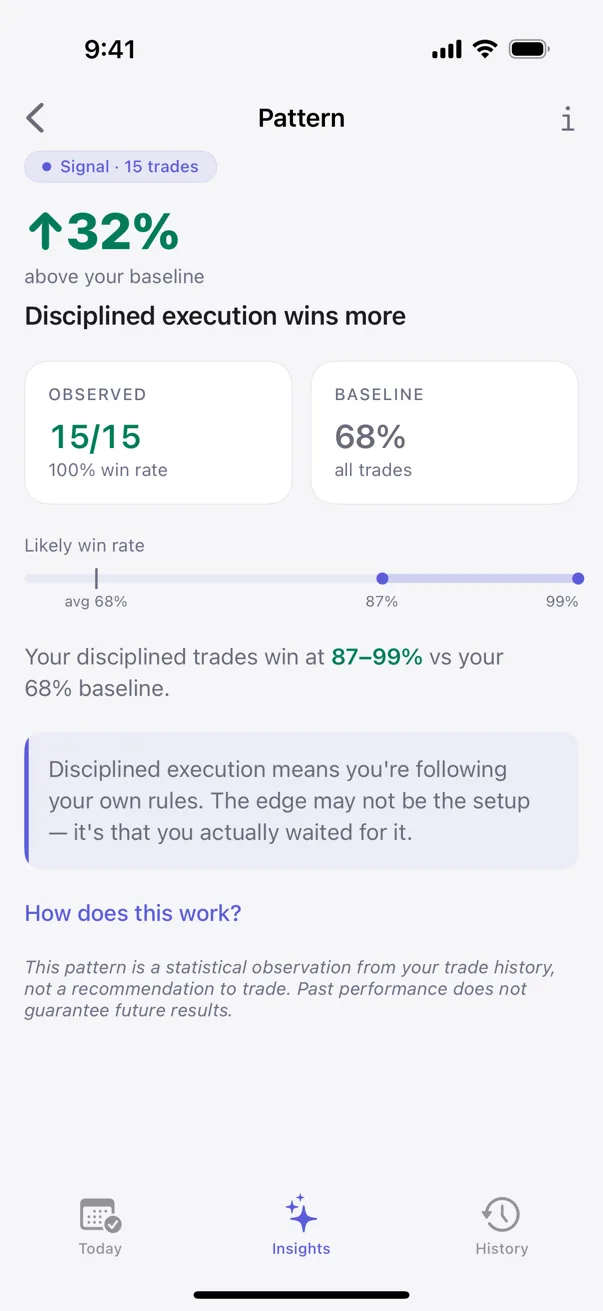

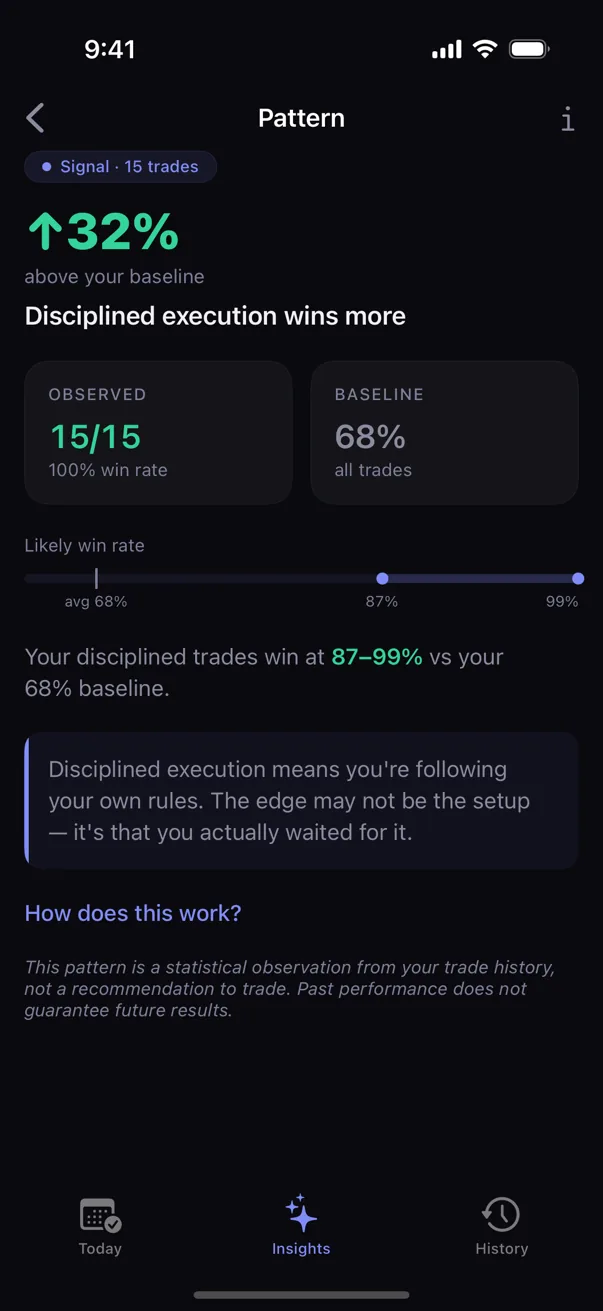

Kyra captures entry price, stated exit plan, and actual exit for each trade. After a sufficient sample, the patterns are visible: do your stops move most often when price approaches them? Do exits cluster at round numbers not present in the plan? Do your longest-held losers show no updated invalidation condition in the log? The answers are in the data, not in self-assessment.

Sources

- Tversky, A., & Kahneman, D. (1974). Judgment under Uncertainty: Heuristics and Biases. Science, 185(4157), 1124–1131.

- Northcraft, G.B., & Neale, M.A. (1987). Experts, amateurs, and real estate: An anchoring-and-adjustment perspective on property pricing decisions. Organizational Behavior and Human Decision Processes, 39(1), 84–97.

- George, T.J., & Hwang, C.-Y. (2004). The 52-week high and momentum investing. Journal of Finance, 59(5), 2145–2176.

Educational only. Not financial or trading advice. Behavioral patterns described above are observations from the published literature; specific outcomes vary with strategy, market conditions, and individual circumstances.